In a sign of how climate change has captured the world’s attention in recent times, the COP26 climate summit in November 2021 attracted a record 38,500 delegates, including many world leaders who gathered in Glasgow to discuss how best to steer humanity away from future disaster.

While the proceedings were messy at times, and some of the outcomes were criticised for falling short of expectations, our view remains that the summit marked an important step forward in strengthening the international consensus necessary to meet the scale of the climate change threat.

Unlike many other difficult issues that governments face today such as how to deal with resurgent Covid-19 outbreaks, global warming and climate change can be addressed effectively only with coordinated global action over a long term horizon. That requires broad, multilateral consensus on the responses needed to rewire the global economy to reduce greenhouse gas emissions to net zero.

(See Powering Up for Net Zero, What to Expect as the World Gets Warmer, Climate Change – Adapt or Perish and Climate Change – The Low-Carbon Transition.)

The key outcomes from COP26 reinforced our view that strong political momentum is building around climate change, and that a powerful shift in policy and regulation worldwide to cut carbon emissions across all kinds of economic activity will progressively reshape the global economy for years to come.

A welcome surprise: US and China find common ground

In an unexpected development at COP26, the US and China published a joint climate declaration, stating that they “are intent on seizing this critical moment to engage in expanded individual and combined efforts to accelerate the transition to a global net zero economy” – a welcome sign of mutual cooperation amid ongoing tensions between the two countries.

“In the area of climate change, there is more agreement between the US and China than divergence, making it an area with huge potential for our cooperation,” said Xie Zhenhua, China's special envoy for climate change. “As two major powers, both China and the US shoulder international responsibilities and obligations. We need to think big.”

“The US and China have no shortage of differences, but on climate, cooperation is the only way to get things done,” said John Kerry, US special envoy for climate change. “We cannot reach our goals without countries working together, and China and the US in particular, as the two largest emitters in the world, both have to help show the way.”

The US said it intends to fully decarbonise its electricity sector by 2035, while China said it would phase down coal consumption during its 15th Five Year Plan spanning 2026-2030 and make best efforts to accelerate this work.

Also at the summit, India Prime Minister Narendra Modi announced that the country would aim to reach carbon neutrality by 2070 and build 500 gigawatts of renewable energy capacity by 2030 to ensure that half of India’s electricity generation comes from renewable sources.

With India’s announcement, leaders of the world’s biggest economies have now publicly committed to decarbonising their economies over the coming decades. Globally, around 90% of emissions are now covered by net zero targets, according to Climate Action Tracker.

The shape of things to come – large gaps remain that must be plugged

We expect the focus will now quickly shift to how global policymakers plan to deliver on their targets to reach net zero emissions. Businesses and investors will want to see detailed roadmaps on how governments intend to achieve these long term climate goals and adapt their economies to build climate resilience. Without detailed pathways to achieve them, the net zero targets would lack credibility.

A critical component of these plans will be measurable, intermediate targets for emissions reduction well before mid-century – essential to ensure that the ultimate goal of limiting global warming to 1.5°C by the end of the century remains within reach, known as “keeping 1.5°C alive”.

Indeed, many countries do not yet have intermediate targets consistent with their own net-zero pledges, which undermines the credibility of those promises and the world’s collective ability to limit global warming to 1.5°C.

Based on current commitments, global warming is estimated to reach 2.7°C at the end of the century if all countries’ unconditional 2030 pledges are fully implemented and 2.6°C if conditional pledges are also implemented, according to the latest analysis in the 2021 Emissions Gap Report published on 26 October 2021 by the United Nations Environment Programme (UNEP), just before the COP26 summit.

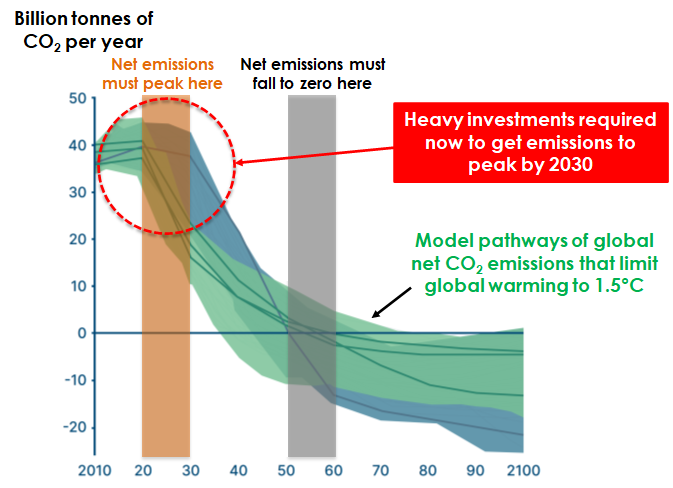

Exhibit 1: To reach net zero emissions by mid-century, key intermediate targets must first be met

Source: Energy Transitions Commission.

Note: Chart shows model pathways for net CO2 emissions that cap global warming at 1.5°C with limited or no overshoot (in green) as well as pathways with higher overshoot (in blue).

Even if all countries’ net-zero emissions pledges are fully implemented, global average temperatures would still rise by around 2.2°C, well above the 1.5°C target, according to the report.

“There is an urgent need for more G20 members – and indeed all countries – to pledge net zero emissions, all countries to increase the robustness of their net-zero pledges, and all net-zero targets to be backed up by near-term actions that give confidence that the net-zero targets can ultimately be achieved,” the report said.

To address this gap, government leaders agreed at the COP26 summit that their ministers will now meet annually starting next year to discuss how to accelerate emissions reduction efforts by 2030.

All countries are also requested to revisit and strengthen their decarbonisation targets by the November 2022 COP27 summit in Egypt. This marks a step forward from the 2015 Paris Agreement, which called on countries to update their pledges only once every five years, and signals greater collective urgency in tackling the climate change threat.

Driving this sense of urgency is mounting scientific evidence that the time left for action is limited, and that the current promises by governments to cut emissions still fall far short of what is needed to limit global warming to 1.5°C.

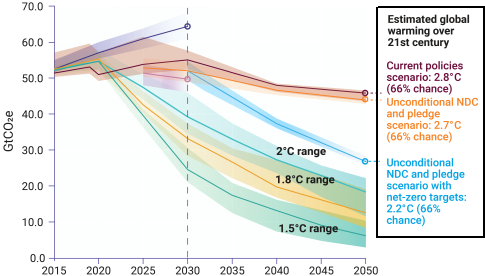

Exhibit 2: Current decarbonisation commitments remain insufficient to limit global warming to 1.5°C, signalling greater policy shifts ahead

Source: UN Emissions Gap Report 2021

Note: NDC = nationally determined contributions, each country’s commitment to reduce greenhouse gas emissions.

A statement issued at the COP26 summit highlighted that “carbon budgets consistent with achieving the Paris Agreement temperature goal are now small and being rapidly depleted”.

The latest assessment of available scientific knowledge on climate change published by the Intergovernmental Panel on Climate Change (IPCC) in August concluded that for a fair (50%) chance of limiting the Earth’s warming to 1.5°C, the remaining carbon budget is estimated to be only 500 GtCO2. (See What to Expect as the World Gets Warmer.)

This is equivalent to just 12.5 years’ worth of emissions at the current pace, based on the estimated 2020 global emissions of 40 GtCO2 by the Global Carbon Project, or less than 10 years’ worth based on the 59.1 GtCO2 emitted in 2019, according to the UNEP’s 2020 Emissions Gap Report.

A strong rebound in emissions is expected in 2021, the UNEP said in its latest (2021) Emissions Gap Report. Preliminary estimates suggest fossil energy CO2 emissions, excluding cement, could rise 4.8% in 2021, and overall global emissions in 2021 are expected to be only slightly lower than the record levels seen in 2019.

New opportunities lie ahead as policy shifts to increase climate ambition

The large remaining emissions gaps – and the narrowing time window available for keeping the 1.5°C target within reach – suggest that policymakers worldwide are likely to strengthen climate policy further over the next few years.

Many key initiatives to accelerate the shift to net zero are already in progress, including efforts to redirect global capital flows towards activities that support climate goals.

Most recently, on 9 November 2021, the People’s Bank of China (PBOC) launched a new lending facility, known as the Carbon Emission Reduction Facility, offering low-cost funds to financial institutions to support the development of clean energy, energy conservation, environmental protection and carbon reduction technology.

“The launch of the facility sends a clear policy signal. It is designed to enhance financial institutions’ awareness of the importance of green transition, encourage more social capital to support the green and low-carbon industries, and to advocate the philosophy of green living, green production and circular economy, which will help achieve the carbon peaking and carbon neutrality goals,” the PBOC said.

The new facility is also likely to encourage the development and refinement of climate reporting in China, as financial institutions will be required to disclose information on lending aimed at cutting carbon emissions, and the amount of emissions reduction supported by such lending.

China has also started building the world’s largest green hydrogen project, to be powered entirely by solar energy.

Other initiatives are also in progress that are likely to shape global climate policy for years to come.

China and the EU are working together to identify a list of economic activities that are recognised by both as green activities. An initial Common Ground Taxonomy focusing on activities that contribute to climate change mitigation across six sectors – energy, manufacturing, construction, transportation, solid waste management and forestry – was published on 4 November 2021.

The document reflects key highlights in both China’s and EU green taxonomies and is expected to support China-EU green finance cooperation and mobilise cross-border climate financing by lowering the green certification cost for cross-border transactions, the PBOC said. It could also be used as a reference by market participants for issuing or trading green financial products.

In October, the White House published a report outlining a government-wide strategy to enhance the US economy’s climate resilience and manage climate-related risks. The strategy outlined in the report is consistent with our view at the start of 2021 that President Joe Biden would likely take a whole-of-government approach to fighting climate change. (See US Re-enters Global Fight Against Climate Change.)

And in Europe, a massive, system-wide transformation of the European Union economy is underway to cut net greenhouse gas emissions across all 27 EU member states by 55% or more by 2030 from 1990 levels, and to net zero by 2050. (See Big Strides Forward on Climate Action.)

As we look ahead into 2022 and beyond, we reiterate our longstanding view that global efforts to strengthen climate ambition and pursue sustainable, climate-resilient development paths will drive profound structural changes to the global economy for years to come.

Even as political leaders continue to grapple with other challenges such as resurgent Covid-19 outbreaks, the longer term policy trajectory is unmistakeable – the world is heading towards a low-carbon economy, because it must.

While the path ahead looks far from smooth, we fully expect efforts to pursue sustainable and climate-friendly economic growth will progressively reshape the world economy over the coming decades, ushering in a new era of opportunities for businesses that successfully adapt to this brave new world.

This will create both significant disruption and new opportunities for businesses as supporting regulations and policy incentives are progressively rolled out globally.

(See What to Expect as the World Gets Warmer, Big Strides Forward on Climate Action, The Narrow Path to Net Zero, Climate Commitments Intensify Globally, Climate Action: At A Tipping Point, US Re-enters Global Fight Against Climate Change and Climate Change – The Low-Carbon Transition).

Increasingly, we see new opportunities emerging in clean energy technologies such as hydrogen, which is attractive as a low-carbon energy source to decarbonise a wide range of economic activity such as power generation, transport, and heating and power for buildings.

We continue to advocate a prudent strategy of adding diversified exposure to a wide range of potential beneficiaries of the global transition to a carbon neutral economy, given the all-encompassing nature of decarbonisation efforts worldwide, and the fast-evolving but uneven deployment of supporting policies and regulations across the world.

Disclaimers and Disclosures

This material is prepared by Bank of Singapore Limited (Co Reg. No.: 197700866R) (the “Bank”) and is distributed in Singapore by the Bank.

This material does not provide individually tailored investment advice. This material has been prepared for and is intended for general circulation. The contents of this material does not take into account the specific investment objectives, investment experience, financial situation, or particular needs of any particular person. You should independently evaluate the contents of this material, and consider the suitability of any product discussed in this material, taking into account your own specific investment objectives, investment experience, financial situation and particular needs. If in doubt about the contents of this material or the suitability of any product discussed in this material, you should obtain independent financial advice from your own financial or other professional advisers, taking into account your specific investment objectives, investment experience, financial situation and particular needs, before making a commitment to purchase any product.

This material is not and should not be construed, by itself, as an offer or a solicitation to deal in any product or to enter into any legal relations. You should contact your own licensed representative directly if you are interested in buying or selling any product discussed in this material.

This material is not intended for distribution, publication or use by any person in any jurisdiction outside Singapore, Hong Kong or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank or its related corporations, connected persons, associated persons or affiliates (collectively “Affiliates”) to any licensing, registration or other requirements in such jurisdiction.

The Bank and its Affiliates may have issued other reports, analyses, or other documents expressing views different from the contents of this material, and may provide other advice or make investment decisions that are contrary to the views expressed in this material, and all views expressed in all reports, analyses and documents are subject to change without notice. The Bank and its Affiliates reserve the right to act upon or use the contents of this material at any time, including before its publication.

The author of this material may have discussed the information or views contained in this material with others within or outside the Bank, and the author or such other Bank employees may have already acted on the basis of such information or views (including communicating such information or views to other customers of the Bank).

The Bank, its employees (including those with whom the author may have consulted in the preparation of this material))and discretionary accounts managed by the Bank may have long or short positions (including positions that may be different from or opposing to the views in this material or may be otherwise interested in any of the product(s) (including derivatives thereof) discussed in material, may have acquired such positions at prices and market conditions that are no longer available, may from time to time deal in such product(s) and may have interests different from or adverse to your interests.

Analyst Declaration

The analyst(s) who prepared this material certifies that the opinions contained herein accurately and exclusively reflect his or her views about the securities of the company(ies) and that he or she has taken reasonable care to maintain independence and objectivity in respect of the opinions herein.

The analyst(s) who prepared this material and his/her associates do not have financial interests in the company(ies). Financial interests refer to investments in securities, warrants and/or other derivatives. The analyst(s) receives compensation based on the overall revenues of Bank of Singapore Limited, and no part of his or her compensation was, is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this material. The reporting line of the analyst(s) is separate from and independent of the business solicitation or marketing departments of Bank of Singapore Limited.

The analyst(s) and his/her associates confirm that they do not serve as directors or officers of the company(ies) and the company(ies)or other third parties have not provided or agreed to provide any compensation or other benefits to the analyst(s) in connection with this material.

An “associate” is defined as (i) the spouse, parent or step-parent, or any minor child (natural or adopted) or minor step-child, or any sibling or step-sibling of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, parent or step-parent, minor child (natural or adopted) or minor step-child, or sibling or step-sibling is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Conflict of Interest Declaration

The Bank is a licensed bank regulated by the Monetary Authority of Singapore in Singapore. Bank of Singapore Limited, Hong Kong Branch (incorporated in Singapore with limited liability), is an Authorized Institution as defined in the Banking Ordinance of Hong Kong (Cap 155), regulated by the Hong Kong Monetary Authority in Hong Kong and a Registered Institution as defined in the Securities and Futures Ordinance of Hong Kong (Cap.571) regulated by the Securities and Futures Commission in Hong Kong. The Bank, its employees and discretionary accounts managed by its Singapore Office/Hong Kong Office may have long or short positions or may be otherwise interested in any of the investment products (including derivatives thereof) referred to in this document and may from time to time dispose of any such investment products. The Bank forms part of the OCBC Group (being for this purpose Oversea-Chinese Banking Corporation Limited (“OCBC Bank”) and its subsidiaries, related and affiliated companies). OCBC Group, their respective directors and/or employees (collectively “Related Persons”) may have interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. OCBC Group and its Related Persons may also be related to, and receive fees from, providers of such investment products. There may be conflicts of interest between OCBC Bank, the Bank, OCBC Investment Research Private Limited, OCBC Securities Private Limited or other members of the OCBC Group and any of the persons or entities mentioned in this report of which the Bank and its analyst(s) are not aware due to OCBC Bank’s Chinese Wall arrangement.

The Bank adheres to a group policy (as revised and updated from time to time) that provides how entities in the OCBC Group manage or eliminate any actual or potential conflicts of interest which may impact the impartiality of research reports issued by any research analyst in the OCBC Group.

If this material pertains to an offer, it may only be offered (i) in Hong Kong, to qualified Private Banking Customers and Professional Investors (as defined under the Securities and Futures Ordinance); (ii) in Singapore, to Accredited Investors (as defined under the Securities and Futures Act 2001); and (iii) in the Dubai International Financial Center, to Professional Clients (as defined under the Dubai Financial Services Authority rules). No other persons may act on the contents of the material.

Other Disclosures

Singapore

Where this material relates to structured deposits, this clause applies:

The product is a structured deposit. Structured deposits are not insured by the Singapore Deposit Insurance Corporation. Unlike traditional deposits, structured deposits have an investment element and returns may vary. You may wish to seek independent advice from a financial adviser before making a commitment to purchase this product. In the event that you choose not to seek independent advice from a financial adviser, you should carefully consider whether this product is suitable for you.

Where this material relates to dual currency investments, this clause applies:

The product is a dual currency investment. A dual currency investment product (“DCI”) is a derivative product or structured product with derivatives embedded in it. A DCI involves a currency option which confers on the deposit-taking institution the right to repay the principal sum at maturity in either the base or alternate currency. Part or all of the interest earned on this investment represents the premium on this option.

By purchasing this DCI, you are giving the issuer of this product the right to repay you at a future date in an alternate currency that is different from the currency in which your initial investment was made, regardless of whether you wish to be repaid in this currency at that time. DCIs are subject to foreign exchange fluctuations which may affect the return of your investment. Exchange controls may also be applicable to the currencies your investment is linked to. You may incur a loss on your principal sum in comparison with the base amount initially invested. You may wish to seek advice from a financial adviser before making a commitment to purchase this product. In the event that you choose not to seek advice from a financial adviser, you should carefully consider whether this product is suitable for you.

Hong Kong

This document has not been delivered for registration to the Registrar of Companies in Hong Kong and its contents have not been reviewed by any regulatory authority in Hong Kong. Accordingly: (i) the shares/notes may not be offered or sold in Hong Kong by means of any document other than to persons who are "Professional Investors" within the meaning of the Securities and Futures Ordinance (Cap. 571) of Hong Kong and the Securities and Futures (Professional Investor) Rules made thereunder or in other circumstances which do not result in the document being a "prospectus" within the meaning of the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Cap. 32) of Hong Kong or which do not constitute an offer to the public within the meaning of the Companies (Winding Up and Miscellaneous Provisions) Ordinance; and (ii) no person may issue any invitation, advertisement or other document relating to the shares/notes whether in Hong Kong or elsewhere, which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong (except if permitted to do so under the securities laws of Hong Kong) other than with respect to the shares/notes which are or are intended to be disposed of only to persons outside Hong Kong or only to "Professional Investors" within the meaning of the Securities and Futures Ordinance and the Securities and Futures (Professional Investor) Rules made thereunder.

The product may involve derivatives. Do not invest in it unless you fully understand and are willing to assume the risks associated with it. If you have any doubt, you should seek independent professional financial, tax and/or legal advice as you deem necessary.

Where this material relates to a Complex Product, this clause applies:

Warning Statement and Information about Complex Product

(Applicable to accounts managed by Hong Kong Relationship Manager)

Where this material relates to a Complex Product – funds and ETFs, this clause applies additionally:

Where this material relates to a Complex Product (Options and its variants, Swap and its variants, Accumulator and its variants, Reverse Accumulator and its variants, Forwards), this clause applies additionally:

Where this material relates to a Loss Absorption Product, this clause applies:

Warning Statement and Information about Loss Absorption Products

(Applicable to accounts managed by Hong Kong Relationship Manager)

Before you invest in any Loss Absorption Product (as defined by the Hong Kong Monetary Authority), please read and ensure that you understand the features of a Loss Absorption Product, which may generally have the following features:

Where this material relates to a certificate of deposit, this clause applies:

It is not a protected deposit and is not protected by the Deposit Protection Scheme in Hong Kong.

Where this material relates to a structured deposit, this clause applies:

It is not a protected deposit and is not protected by the Deposit Protection Scheme in Hong Kong.

Where this material relates to a structured product, this clause applies:

This is a structured product which involves derivatives. Do not invest in it unless you fully understand and are willing to assume the risks associated with it. If you are in any doubt about the risks involved in the product, you may clarify with the intermediary or seek independent professional advice.

Dubai International Financial Center

Where this material relates to structured products and bonds, this clause applies:

The Distributor represents and agrees that it has not offered and will not offer the product to any person in the Dubai International Financial Centre unless such offer is an “Exempt Offer” in accordance with the Market Rules of the Dubai Financial Services Authority (the “DFSA”).

The DFSA has no responsibility for reviewing or verifying any documents in connection with Exempt Offers.

The DFSA has not approved the Information Memorandum or taken steps to verify the information set out in it, and has no responsibility for it.

The product to which this document relates may be illiquid and/or subject to restrictions in respect of their resale. Prospective purchasers of the products offered should conduct their own due diligence on the products.

Please make sure that you understand the contents of the relevant offering documents (including but not limited to the Information Memorandum or Offering Circular) and the terms set out in this document. If you do not understand the contents of the relevant offering documents and the terms set out in this document, you should consult an authorised financial adviser as you deem necessary, before you decide whether or not to invest.

Where this material relates to a fund, this clause applies:

This Fund is not subject to any form of regulation or approval by the Dubai Financial Services Authority (“DFSA”). The DFSA has no responsibility for reviewing or verifying any Prospectus or other documents in connection with this Fund. Accordingly, the DFSA has not approved the Prospectus or any other associated documents nor taken any steps to verify the information set out in the Prospectus, and has no responsibility for it. The Units to which this Fund relates may be illiquid and/or subject to restrictions on their resale. Prospective purchasers should conduct their own due diligence on the Units. If you do not understand the contents of this document you should consult an authorized financial adviser. Please note that this offer is intended for only Professional Clients and is not directed at Retail Clients.

These are also available for inspection, during normal business hours, at the following location:

Bank of Singapore

Office 30-34 Level 28

Central Park Tower

DIFC, Dubai

U.A.E

Cross Border Disclaimer and Disclosures

Refer to https://www.bankofsingapore.com/Disclaimers_and_Disclosures.html for cross-border marketing disclaimers and disclosures.