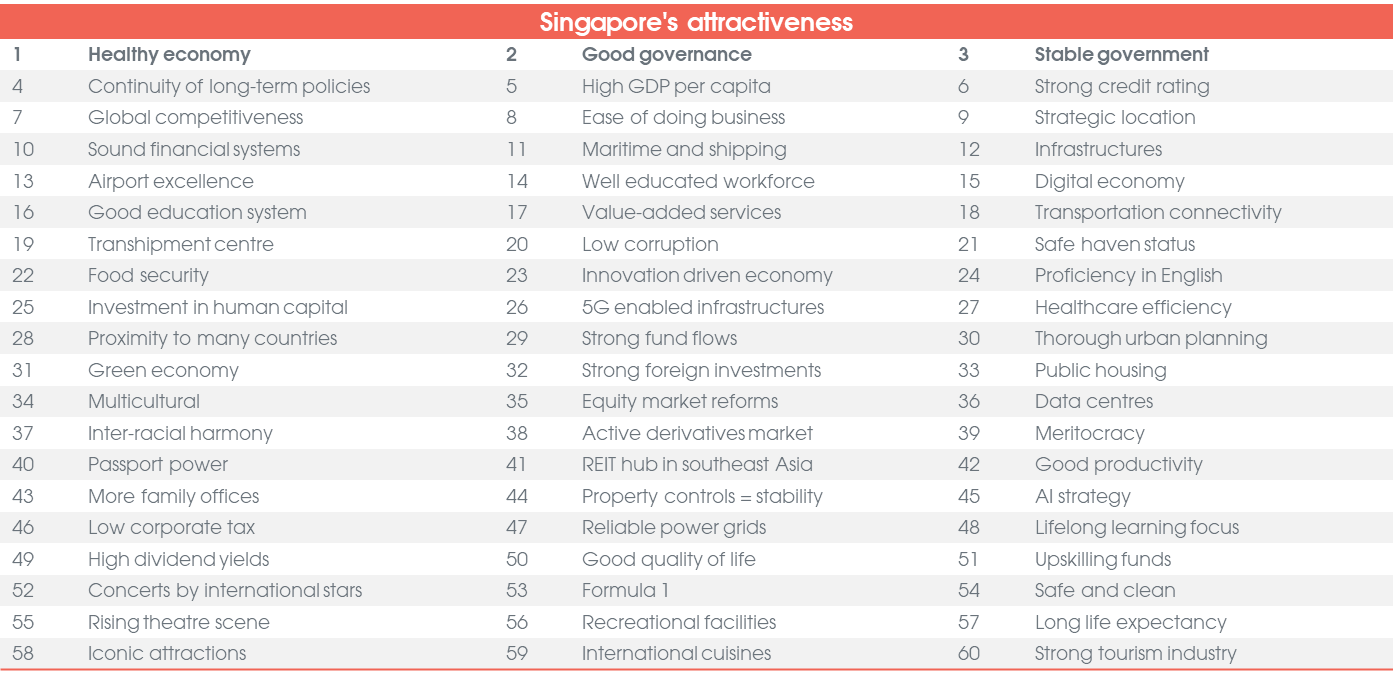

60 reasons to stay invested in Singapore

This year marks the 60th year since Singapore’s independence – from swampland to a thriving metropolis. Singapore has undergone a remarkable transformation in the last 60 years and a host of activities, discounts, promotions and special celebrations have been planned for this year as the nation comes together to celebrate this significant milestone. Retail outlets, grocery stores, restaurants and even places of interests have special packages, and many companies have also planned special events. Although exhibit 1 provides the top 60 reasons to invest in Singapore, there are many other benefits as to why investors should continue to stay invested in Singapore in the coming decade. Singapore’s success in the past 60 years was no pure luck, but rather a carefully planned series of developments and investments that brought Singapore’s focus from textile and then electronics manufacturing in the 60s and 70s to a digital nation now. Moving into the coming decade, the combined regional growth and rising affluence will bring about more opportunities in this region.

Exhibit 1: 60 reasons to stay invested

Source: Bank of Singapore

Singapore’s stability is often stated but has been under-appreciated for a long while

With rising global uncertainty – from elevated geopolitical tensions and higher trade tariffs – stability is increasingly going to be more valuable. Singapore’s economic stability is often over-stated, but at times seems to be under-appreciated. In a climate of rising geopolitical tensions, one of the Singapore’s key investment merits is its economic stability. This is sharpened through years of strategic government initiatives and policies; well-established housing and well-connected infrastructure; and a transparent and robust financial system. The political landscape is stable, with no change to the leading political party since independence. This has allowed for the continuation of several long-term initiatives to enhance infrastructure and develop core skills to meet changing needs.

Providing a safe haven, with Straits Times Index (STI) hitting new historical highs above 4,000

The recent re-rating of the Singapore market was largely fuelled by its safe haven status as seen from the good gains by defensive stocks. The benchmark STI has provided a stable growth of 3.0% per annum over the past 20 years. A safe haven status has not only attracted a constant stream of foreign investments into key industries and recently into the stock market, but it also means that the island will remain a key wealth hub as more family offices and assets flow into the country. Strong foreign investments reinforce the country’s appeal to foreign companies and is also reflective of the confidence of foreign investors despite elevated global uncertainties.

In Asia, the wealth and credit card business is growing. Asia is going to be home to more and more middle-class families due to rising affluence. It is also estimated that Asia will account for more than 50% of the world’s wealthiest people and this is a key indicator for the region. The Asia Pacific region is projected to account for nearly half of all new high net-worth individuals (HNWI) between 2025 and 2028. This will be supported by digital transformation happening throughout Asia, policies encouraging entrepreneurship, higher regional trades and investments.

For the STI, the 4,000 psychological barrier is key, and having convincingly pierced it recently (the STI cracked the 4,000 level on 2 July 2025 and has since stayed above this level despite market volatility), the STI looks likely to hold at current levels, pending no drastic deterioration in the external environment. It is up 10.4% year-to-date (YTD).

A trip back in time showed that the Singapore market capitalisation 20 years ago was USD247b. Now, it is USD502b or a compounded annual growth rate of 3.5%.

High dividend yields – a key differentiator

As a wealth hub and with funds looking for attractive yields in an environment that is likely to see lower interest rates, Singapore listed companies have consistently offered one of the highest dividend yields in this region and globally. The strong SGD also means that foreign investors investing in local equities in SGD terms have enjoyed both good currency gains as well as steady dividend income. With the prohibitive property measures for foreign investors buying into local residential properties, Singapore equities offer a compelling alternative for investors holding SGD. At current levels, the average dividend yield for the STI is 5%. This is attractive for investors looking for stable and sustainable long-term returns.

In the Singapore Treasury bills market, the average auction amount in 2025 was SGD7.4b versus applications of SGD17.5b or a cover ratio of 2.4x. Demand far outstrips supply. The recent auction closed with a cut-off yield of 1.79% (auction results on 17 Jul 2025). As an indication, the cut-off yield was an average of 3.85% in 2023, 3.46% in 2024 to around 2.52% so far this year. However, these rates are still higher than the averages seen pre-Covid at around 0.58% in 2020 and 0.37% in 2021. Meanwhile, the USD has weakened against SGD this year by about 6.1%.

The compounded average growth rate for the STI in the last 20 years was 3.0%. The average dividend yield during the same period was 4%, giving total return of 7.0% – a decent rate of return for the past 20 years.

Global tariffs and geopolitical tensions

In the past few months, the volatile Middle East situation and trade tariffs have rose and ebbed, capturing the dynamic and fluctuating global developments and changes. These have added uncertainty to the investment climate and created both opportunities and challenges. While certain countries are more impacted than others, Singapore has been comparatively less impacted versus the rest of the world. Nevertheless, higher tariff rates for regional countries will still have some spillover effects on certain Singapore companies. However, there is a need to distinguish between noises and signals.

Equity market reforms and initiatives

The Equities Market Review Group provided a progress update recently: an initial tranche of SGD1.1b will be placed with three asset managers under the SGD5b Equity Market Development Program (EQDP), and the Monetary Authority of Singapore (MAS) will appoint more asset managers in the second tranche by 4Q25. Additionally, MAS will also provide SGD50m under the Grant for Equity Markets (GEMS) schedule to strengthen equity research and listing support. We expect quality small/mid-cap stocks, as well as S-REITs, to be potential beneficiaries of these developments. A key risk, in our view, is investor overcrowding in certain small/mid-cap names; if liquidity cannot be maintained over the longer term, especially after funds are fully deployed, small/mid-cap counters trading at frothy valuations without supportive underlying fundamentals could be at risk of sharp drawdowns or profit-taking activity.

Financials

Singapore banks have used structural hedging on their loans books to mitigate the pressure that US Federal Reserve (Fed) rate cuts may place on net interest margins (NIM). Falling interest rates will also help to alleviate asset quality concerns on the banking sector, which plays a pivotal role and accounts for almost 50% of the market capitalisation of the STI.

While rates are generally expected to be lower in 2025 than in 2023-2024, which led to concerns about NIM compression, it is worth noting that pre-Covid interest rates were significantly lower and lower NIM margins are generally expected and already priced in earnings projections.

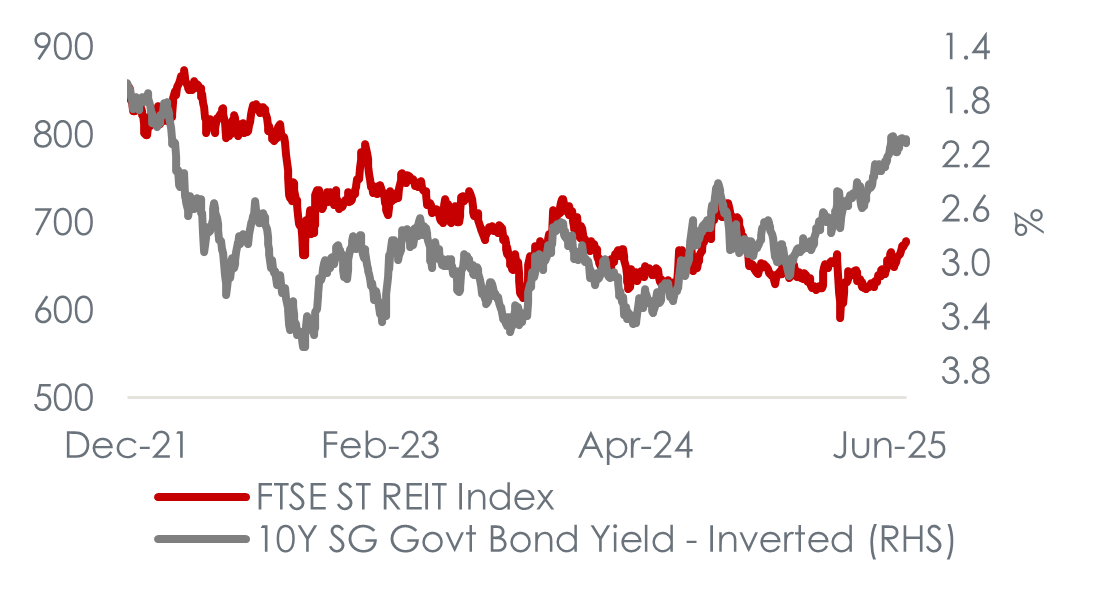

S-REITs

The S-REITs sector has delivered relatively lacklustre returns in recent years, with total returns for the FTSE ST All-Share REIT Index (FSTREI) coming in at -10.7%, +6.5% and -6.2% in 2022, 2023 and 2024 respectively. In contrast, the STI recorded positive total returns in all of those years. Barring any material deterioration in the macroeconomic environment, we believe the S-REITs sector’s drab performance is set to reverse in 2025.

Exhibit 2: Historical trend between FSTREI and Singapore 10Y government yield (inverted)

Source: Bloomberg, internal estimates, as at 29 July 2025

We expect an inflection in distribution per unit (DPU) growth for the S-REITs under our coverage. Some REIT managers have started to guide for improving average debt costs, and continued positive rental reversions (with the exception of some overseas markets such as China) albeit at a moderated pace which will help to reverse DPU growth from negative territory for the current financial year (FY1) to positive territory for the next financial year (FY2), based on our forecasts.

Our preference of the major sub-sectors from most preferred to least preferred is (i) retail, (ii) logistics and industrial (data centres are most preferred within this segment), (iii) office and

(iv) hospitality. We recommend a continued selective stock-picking approach focusing on quality as S-REITs are not immune to the vagaries of the macroeconomic landscape.

Developers/real estate investment managers (REIM)

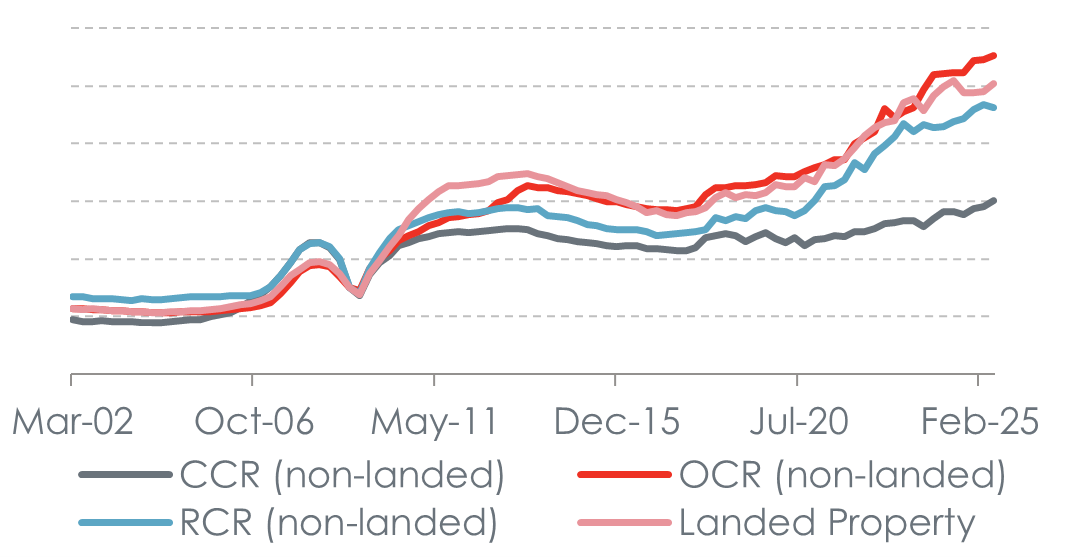

The Singapore residential market has demonstrated notable resilience in price performance. The URA Private Residential Property Price Index (PPI) appreciated 1.8% in 1H25 as compared to end-2024. We forecast private residential property price growth of +2% to +4% in 2025, underpinned by a more favourable interest rate environment, less pessimism on the global economy, higher launch prices of new projects with decent sell-through rates and strong household balance sheets.

We believe property cooling measures remain a key risk. The latest tightening measures came in early July 2025, when the Singapore Government announced the extension of holding period from three years to four years for the payment of Seller’s Stamp Duty (SSD), and raised the SSD rates by 4 percentage points (ppt) for each tier of the holding period. Hence, besides the property development business, developers have also been diversifying their income streams by growing their investment properties portfolio.

REIMs are similarly looking to increase their recurring income streams by growing their funds under management (FUM), which will lead to higher fee income and increase their return on equity (ROE). To achieve their goals, capital recycling will be a key focus of the REIM as they look to monetise their assets and redeploy capital into new economy asset classes.

Exhibit 3: Singapore private residential properties price trend

Source: URA

Industrials

Singapore’s Industrials sector has performed well YTD, and we see three themes playing out for the rest of the year.

First, ongoing tariff uncertainty and rapid policy changes are forcing many companies to adopt a “wait and see” approach and to delay business decisions. In our view, companies with strong balance sheets and a healthy order backlog will be better positioned to tide through this period of volatility. We continue to adopt a cautious stance as a deeper growth slowdown is still very much on the cards for the rest of the year, in our view.

Secondly, defence is likely to remain in vogue given rising geopolitical tensions and President Trump’s use of defence spending as a tariff negotiations tool.

Finally, ongoing market reforms, including the EQDP, may drive a renaissance of small/mid-cap names, a number of which sit within the Industrials sector.

Consumer

According to Singapore Department of Statistics, Singapore retail sales increased 1.4% year-on-year (YoY) in May 2025, continuing the 0.2% growth in April 2025. Retail sales of supermarkets and hypermarkets grew 7.2% YoY or 4.1% month-on-month (MoM) in May 2025, which we believe was largely driven by the distribution of the second tranche of CDC voucher (SGD500) in 2025. Singapore citizens are also entitled to an additional SGD600 or SGD800 CDC vouchers depending on his/her age in 2025 under the SG60 Package to celebrate Singapore’s 60th anniversary of independence.

Conclusion

Singapore equities allow the investor to gain exposure to a healthy economy known for its strong governance, political stability and robust financial regulations. Singapore equities provide geographic diversification, and relative defensiveness during times of uncertainties and this will help to reduce overall portfolio risks. The attractive dividend yields are appealing to income-focused investors, while discerning investors could discover growth opportunities. Exposure to the Singapore dollar (SGD) through Singapore equities adds a currency diversification benefit which could hedge against volatility in other currencies.

Disclaimers and Disclosures

This material is prepared by Bank of Singapore Limited (Co Reg. No.: 197700866R) (the “Bank”) and is distributed in Singapore by the Bank.

This material does not provide individually tailored investment advice. This material has been prepared for and is intended for general circulation. The contents of this material does not take into account the specific investment objectives, investment experience, financial situation, or particular needs of any particular person. You should independently evaluate the contents of this material, and consider the suitability of any product discussed in this material, taking into account your own specific investment objectives, investment experience, financial situation and particular needs. If in doubt about the contents of this material or the suitability of any product discussed in this material, you should obtain independent financial advice from your own financial or other professional advisers, taking into account your specific investment objectives, investment experience, financial situation and particular needs, before making a commitment to purchase any product.

The Bank shall not be responsible or liable for any loss (whether direct, indirect or consequential) that may arise from, or in connection with, any use of or reliance on any information contained in or derived from this material, or any omission from this material, other than where such loss is caused solely by the Bank’s wilful default or gross negligence.

This material is not and should not be construed, by itself, as an offer or a solicitation to deal in any product or to enter into any legal relations. You should contact your own licensed representative directly if you are interested in buying or selling any product discussed in this material.

This material is not intended for distribution, publication or use by any person in any jurisdiction outside Singapore, Hong Kong or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank or its related corporations, connected persons, associated persons or affiliates (collectively “Affiliates”) to any licensing, registration or other requirements in such jurisdiction.

The Bank and its Affiliates may have issued other reports, analyses, or other documents expressing views different from the contents of this material, and may provide other recommendations or make investment decisions that are contrary to the views expressed in this material, and all views expressed in all reports, analyses and documents are subject to change without notice. The Bank and its Affiliates reserve the right to act upon or use the contents of this material at any time, including before its publication.

The author of this material may have discussed the information or views contained in this material with others within or outside the Bank, and the author or such other Bank employees may have already acted on the basis of such information or views (including communicating such information or views to other customers of the Bank).

The Bank, its employees (including those with whom the author may have consulted in the preparation of this material))and discretionary accounts managed by the Bank may have long or short positions (including positions that may be different from or opposing to the views in this material or may be otherwise interested in any of the product(s) (including derivatives thereof) discussed in material, may have acquired such positions at prices and market conditions that are no longer available, may from time to time deal in such product(s) and may have interests different from or adverse to your interests.

Analyst Declaration

The analyst(s) who prepared this material certifies that the opinions contained herein accurately and exclusively reflect his or her views about the securities of the company(ies) and that he or she has taken reasonable care to maintain independence and objectivity in respect of the opinions herein.

The analyst(s) who prepared this material and his/her associates do not have financial interests in the company(ies). Financial interests refer to investments in securities, warrants and/or other derivatives. The analyst(s) receives compensation based on the overall revenues of Bank of Singapore Limited, and no part of his or her compensation was, is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this material. The reporting line of the analyst(s) is separate from and independent of the business solicitation or marketing departments of Bank of Singapore Limited.

The analyst(s) and his/her associates confirm that they do not serve as directors or officers of the company(ies) and the company(ies)or other third parties have not provided or agreed to provide any compensation or other benefits to the analyst(s) in connection with this material.

An “associate” is defined as (i) the spouse, parent or step-parent, or any minor child (natural or adopted) or minor step-child, or any sibling or step-sibling of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, parent or step-parent, minor child (natural or adopted) or minor step-child, or sibling or step-sibling is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Conflict of Interest Declaration

The Bank is a licensed bank regulated by the Monetary Authority of Singapore in Singapore. Bank of Singapore Limited, Hong Kong Branch (incorporated in Singapore with limited liability), is an Authorized Institution as defined in the Banking Ordinance of Hong Kong (Cap 155), regulated by the Hong Kong Monetary Authority in Hong Kong and a Registered Institution as defined in the Securities and Futures Ordinance of Hong Kong (Cap.571) regulated by the Securities and Futures Commission in Hong Kong. The Bank, its employees and discretionary accounts managed by its Singapore Office/Hong Kong Office may have long or short positions or may be otherwise interested in any of the investment products (including derivatives thereof) referred to in this document and may from time to time dispose of any such investment products. The Bank forms part of the OCBC Group (being for this purpose Oversea-Chinese Banking Corporation Limited (“OCBC Bank”) and its subsidiaries, related and affiliated companies). OCBC Group, their respective directors and/or employees (collectively “Related Persons”) may have interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. OCBC Group and its Related Persons may also be related to, and receive fees from, providers of such investment products. There may be conflicts of interest between OCBC Bank, the Bank, OCBC Investment Research Private Limited, OCBC Securities Private Limited or other members of the OCBC Group and any of the persons or entities mentioned in this report of which the Bank and its analyst(s) are not aware due to OCBC Bank’s Chinese Wall arrangement.

The Bank adheres to a group policy (as revised and updated from time to time) that provides how entities in the OCBC Group manage or eliminate any actual or potential conflicts of interest which may impact the impartiality of research reports issued by any research analyst in the OCBC Group.

Other Disclosures

Dubai International Financial Center (DIFC)

Where this material relates to structured products and bonds, this clause applies:

The Distributor represents and agrees that it has not offered and will not offer the product to any person in the Dubai International Financial Centre unless such offer is an “Exempt Offer” in accordance with the Market Rules of the Dubai Financial Services Authority (the “DFSA”).

The DFSA has no responsibility for reviewing or verifying any documents in connection with Exempt Offers.

The DFSA has not approved the Information Memorandum or taken steps to verify the information set out in it, and has no responsibility for it.

The product to which this document relates may be illiquid and/or subject to restrictions in respect of their resale. Prospective purchasers of the products offered should conduct their own due diligence on the products.

Please make sure that you understand the contents of the relevant offering documents (including but not limited to the Information Memorandum or Offering Circular) and the terms set out in this document. If you do not understand the contents of the relevant offering documents and the terms set out in this document, you should consult an authorised financial adviser as you deem necessary, before you decide whether or not to invest.

Where this material relates to a fund, this clause applies:

This Fund is not subject to any form of regulation or approval by the Dubai Financial Services Authority (“DFSA”). The DFSA has no responsibility for reviewing or verifying any Prospectus or other documents in connection with this Fund. Accordingly, the DFSA has not approved the Prospectus or any other associated documents nor taken any steps to verify the information set out in the Prospectus, and has no responsibility for it. The Units to which this Fund relates may be illiquid and/or subject to restrictions on their resale. Prospective purchasers should conduct their own due diligence on the Units. If you do not understand the contents of this document you should consult an authorized financial adviser. Please note that this offer is intended for only Professional Clients and is not directed at Retail Clients.

These are also available for inspection, during normal business hours, at the following location:

Bank of Singapore

Office 30-34 Level 28

Central Park Tower

DIFC, Dubai

U.A.E

Hong Kong

Bank of Singapore Limited (Hong Kong Branch) is an Authorized Institution as defined in the Banking Ordinance of Hong Kong (Cap 155), regulated by the Hong Kong Monetary Authority in Hong Kong and a Registered Institution as defined in the Securities and Futures Ordinance of Hong Kong (Cap.571). Financial products and services are only offered to “Professional Investors" within the meaning of the Securities and Futures Ordinance and the Securities and Futures (Professional Investor) Rules made thereunder.

This material has not been delivered for registration to the Registrar of Companies in Hong Kong and its contents have not been reviewed by any regulatory authority in Hong Kong. Accordingly: (i) the investment product may not be offered or sold in Hong Kong by means of any document other than to persons who are "Professional Investors" within the meaning of the Securities and Futures Ordinance (Cap. 571) of Hong Kong and the Securities and Futures (Professional Investor) Rules made thereunder or in other circumstances which do not result in the document being a "prospectus" within the meaning of the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Cap. 32) of Hong Kong or which do not constitute an offer to the public within the meaning of the Companies (Winding Up and Miscellaneous Provisions) Ordinance; and (ii) no person may issue any invitation, advertisement or other material relating to the investment product whether in Hong Kong or elsewhere, which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong (except if permitted to do so under the securities laws of Hong Kong) other than with respect to the investment product which is or is intended to be disposed of only to persons outside Hong Kong or only to "Professional Investors" within the meaning of the Securities and Futures Ordinance and the Securities and Futures (Professional Investor) Rules made thereunder.

Where this material involves derivatives, do not invest in it unless you fully understand and are willing to assume the risks associated with it. If you have any doubt, you should seek independent professional financial, tax and/or legal advice as you deem necessary.

Where this material relates to a Complex Product, this clause applies:

Warning Statement and Information about Complex Product

(Applicable to accounts managed by Hong Kong Relationship Managers)

Where this material relates to a Complex Product (funds and ETFs), this clause applies additionally:

Where this material relates to a Complex Product (Options and its variants, Swap and its variants, Accumulator and its variants, Reverse Accumulator and its variants, Forwards), this clause applies additionally:

Where this material relates to a Loss Absorption Product, this clause applies:

Warning Statement and Information about Loss Absorption Products

(Applicable to accounts managed by Hong Kong Relationship Managers)

Before you invest in any Loss Absorption Product (as defined by the Hong Kong Monetary Authority), please read and ensure that you understand the features of a Loss Absorption Product, which may generally have the following features:

Where this material relates to a certificate of deposit, this clause applies:

A certificate of deposit is not a protected deposit and is not protected by the Deposit Protection Scheme in Hong Kong.

Where this material relates to a structured deposit, this clause applies:

A structured deposit is not a protected deposit and is not protected by the Deposit Protection Scheme in Hong Kong.

Where this material relates to a structured product, this clause applies:

This is a structured product which involves derivatives. Do not invest in it unless you fully understand and are willing to assume the risks associated with it. If you are in any doubt about the risks involved in the product, you may clarify with the intermediary or seek independent professional advice.

Singapore

Bank of Singapore Limited is a bank licensed and regulated by the Monetary Authority of Singapore. The Bank is also an Exempt Capital Markets Services Entity under the Securities and Futures Act 2001 and an Exempt Financial Adviser under the Financial Advisers Act 2001.

Where this material relates to structured deposits, this clause applies:

The product is a structured deposit. Structured deposits are not insured by the Singapore Deposit Insurance Corporation. Unlike traditional deposits, structured deposits have an investment element and returns may vary. You may wish to seek independent advice from a financial adviser before making a commitment to purchase this product. In the event that you choose not to seek independent advice from a financial adviser, you should carefully consider whether this product is suitable for you.

Where this material relates to dual currency investments, this clause applies:

The product is a dual currency investment. A dual currency investment product (“DCI”) is a derivative product or structured product with derivatives embedded in it. A DCI involves a currency option which confers on the deposit-taking institution the right to repay the principal sum at maturity in either the base or alternate currency. Part or all of the interest earned on this investment represents the premium on this option.

By purchasing this DCI, you are giving the issuer of this product the right to repay you at a future date in an alternate currency that is different from the currency in which your initial investment was made, regardless of whether you wish to be repaid in this currency at that time. DCIs are subject to foreign exchange fluctuations which may affect the return of your investment. Exchange controls may also be applicable to the currencies your investment is linked to. You may incur a loss on your principal sum in comparison with the base amount initially invested. You may wish to seek advice from a financial adviser before making a commitment to purchase this product. In the event that you choose not to seek advice from a financial adviser, you should carefully consider whether this product is suitable for you.

United Kingdom

Bank of Singapore Limited, UK Branch (BOSL UK) is incorporated and registered in Singapore with the Accounting and Corporate Regulatory Authority (Registration no.:197700866R) as a public company limited by shares with head office in Singapore and operating in the UK through its UK establishment (BR027666). Bank of Singapore Limited, UK branch (FRN: 1038970) is an appointed representative of Oversea-Chinese Banking Corporation Limited, London branch. Oversea-Chinese Banking Corporation Limited (OCBC) is authorised and regulated by the Monetary Authority of Singapore. OCBC London Branch is authorised by the Prudential Regulation Authority with firm reference number 204687 and subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of OCBC London Branch’s regulation by the Prudential Regulation Authority are available on request. This material is intended solely for the use of the designated recipients. Unauthorised access, use, or distribution is strictly prohibited. If you are not the intended recipient, please notify us immediately and erase all copies. Bank of Singapore Limited, UK Branch does not provide legal, accounting or tax advice. Please consult an independent professional for advice tailored to your specific situation.

This product or service is offered exclusively for investors eligible for categorisation as a professional client. This is not intended for retail clients. Any person in the UK who receives this material is deemed to have represented and agreed that they qualify as a Professional Client. Such recipients also represent and agree that they have not received this material on behalf of any persons in the UK other than Professional Clients for whom they have authority to make investment decisions on a wholly discretionary basis. BOSL UK will rely on the truth and accuracy of these representations and agreements. Any person who is not a Professional Client should neither act on nor rely upon this material or any of its contents.

Investing in financial markets carries the risk of losing capital, and investors should be aware of and carefully consider this risk before making any investment decisions. The value of investments can fluctuate, and there is no guarantee that investors will recoup their initial investment. Past performance is not indicative of future results, and the performance of investments can be affected by various factors, including but not limited to market conditions, economic factors, and changes in regulations or tax laws. Forward-looking statements should not be considered as guarantees or predictions of future events. Investors should be prepared for the possibility of losing all or a portion of their invested capital. It is recommended that investors seek professional advice and conduct thorough research before making any investment decisions. BOSL UK does not endorse any specific investments or financial products mentioned in this material. Neither BOSL UK nor its employees accept any liability for any loss or damage arising from the use of this material or reliance on its content.

Cross Border Disclaimer and Disclosures

Refer to https://www.bankofsingapore.com/Disclaimers_and_Disclosures.html for cross-border marketing disclaimers and disclosures.

ESG Disclaimer

This document contains information on ESG factors or the Bank’s process for taking into consideration, and evaluation or assessment of ESG factors.

There are currently no universally accepted environmental, social and governance (“ESG”) standards, and no consensus as to whether activities and practices or products or services are “environmentally friendly”, “sustainable”, “responsible”, “climate friendly”, etc. Evaluation of ESG outcomes or metrics may require forward-looking scenario analysis, estimates, interpretations and assumptions and may be uncertain and speculative. There may not be scientific consensus. Scientific evidence and data may not be conclusive or there may be limitations, and new evidence and data may be emerging. ESG standards may depend on subjective or value judgments. ESG standards, as well as laws, rules and regulations may differ from jurisdiction to jurisdiction. Taxonomies have been developed in different jurisdictions to classify activities as “environmentally sustainable”, “green” or the equivalent, and different taxonomies may classify the same activity differently. Achieving one ESG goal may be at the expense of, or require a compromise on, other ESG goals. The Bank’s ESG standards and evaluation or assessment of ESG factors may therefore not meet your expectations or objectives and may not be consistent with certain ESG laws, rules, regulations and standards. There is no guarantee that there will not be negative ESG outcomes, and the Bank does not give any assurance that your investments will have a positive ESG impact. You should ensure that you understand the Bank’s ESG standards and process for evaluation or assessment of ESG factors, and assess whether the Bank’s ESG standards and process for evaluation or assessment of ESG factors meets your expectations or is appropriate for you, before making any investment commitment. You are solely responsible for your own investment decisions.

The Bank relies on third party ESG ratings. While the Bank has selected its third party ESG rating providers in good faith and with reasonable care, the Bank has not independently verified the ESG ratings of third party providers. The Bank gives no representation or warranty, express or implied, as to the quality, accuracy, completeness, rigour, timeliness or verifiability of such third party ESG ratings, and shall not be responsible or liable for such third party ESG ratings. ESG ratings may be based on data that is incomplete, due to limitations or otherwise, or based on commitments and targets which may not be achieved. You should review and understand the disclosures made by such third party ESG ratings providers on their methodologies, data sources and other relevant information, and obtain advice from professional advisers as necessary.

Taking into consideration ESG factors may be at the expense of higher financial returns, especially in the short term. Although ESG risks may result in financial losses, such losses may, and if at all, only materialise in the long term. ESG factors and screening may also result in certain investments that deliver high financial returns being excluded, or limit the diversity of investments, which could in turn affect the volatility of portfolios.