Framing the challenge

Equity portfolios built around global market-cap benchmarks no longer reflect the shape of the world to come. What is often treated as a neutral allocation embeds specific structural exposures – to US dominance, tech-led growth, and USD strength – that are increasingly regime-dependent. This paper sets out a regionally structured equity sleeve as a more balanced and resilient way to express long-term equity exposure, informed by robust methodology and aligned with a world that is fragmenting along economic, geopolitical, and institutional lines.

The problem with status quo

Market-cap weighting remains the default option in global equity allocation. Its appeal lies in its ease of use, which is why it is the most prevalently applied approach to create portfolio benchmarks. It reflects the size and liquidity of listed companies, requires limited forecasting, and is straightforward to scale. But the inclination to take such benchmarks as the base case for equity allocation can harden into complacency.

Market-cap indices embed specific exposures that are neither neutral nor static. They concentrate risk in a narrow set of countries, sectors, currencies, and styles – especially US large-cap growth stocks, with dominant weight in technology and unhedged USD exposure. These features were rewarded in the last cycle but are not universally robust across regimes.

A portfolio that tracks market cap expresses an implicit view: that US dominance, tech leadership, and USD strength will persist. These are not constants – they are outcomes of a particular macro-financial environment shaped by globalisation, easy monetary policy, and deflationary bias, all of which are receding.

What is missing is intentionality. Market-cap weighting reflects capital accumulation, not future opportunity. It does not adjust for concentration risk or align with emerging regime shifts. It cannot incorporate forward-looking themes or structural change.

This paper starts from a different premise: portfolios should reflect where the world is going, not just where capital has been deployed. In an environment marked by fragmentation, fiscal drivers, and diverging policies, equity exposure must be more deliberate. The goal is to reframe global equity allocation for greater structural balance and resilience.

Market cap is not neutral: Understanding the concentration

In investment strategy, “neutral” is often shorthand for an allocation that carries no active views – a benchmark exposure that reflects the world as it is. Market-cap weighted indices are typically treated this way: as a neutral representation of global equity opportunity, requiring no further intervention. But neutrality in form is not neutrality in effect.

A market-cap weighted portfolio reflects where capital has accumulated – not necessarily where future returns are most likely, nor where risk is best diversified. It is the outcome of past price movements and capital flows, shaped by prevailing trends in monetary policy, globalisation, and technology. What appears passive is, in fact, a concentrated expression of specific macro and market conditions.

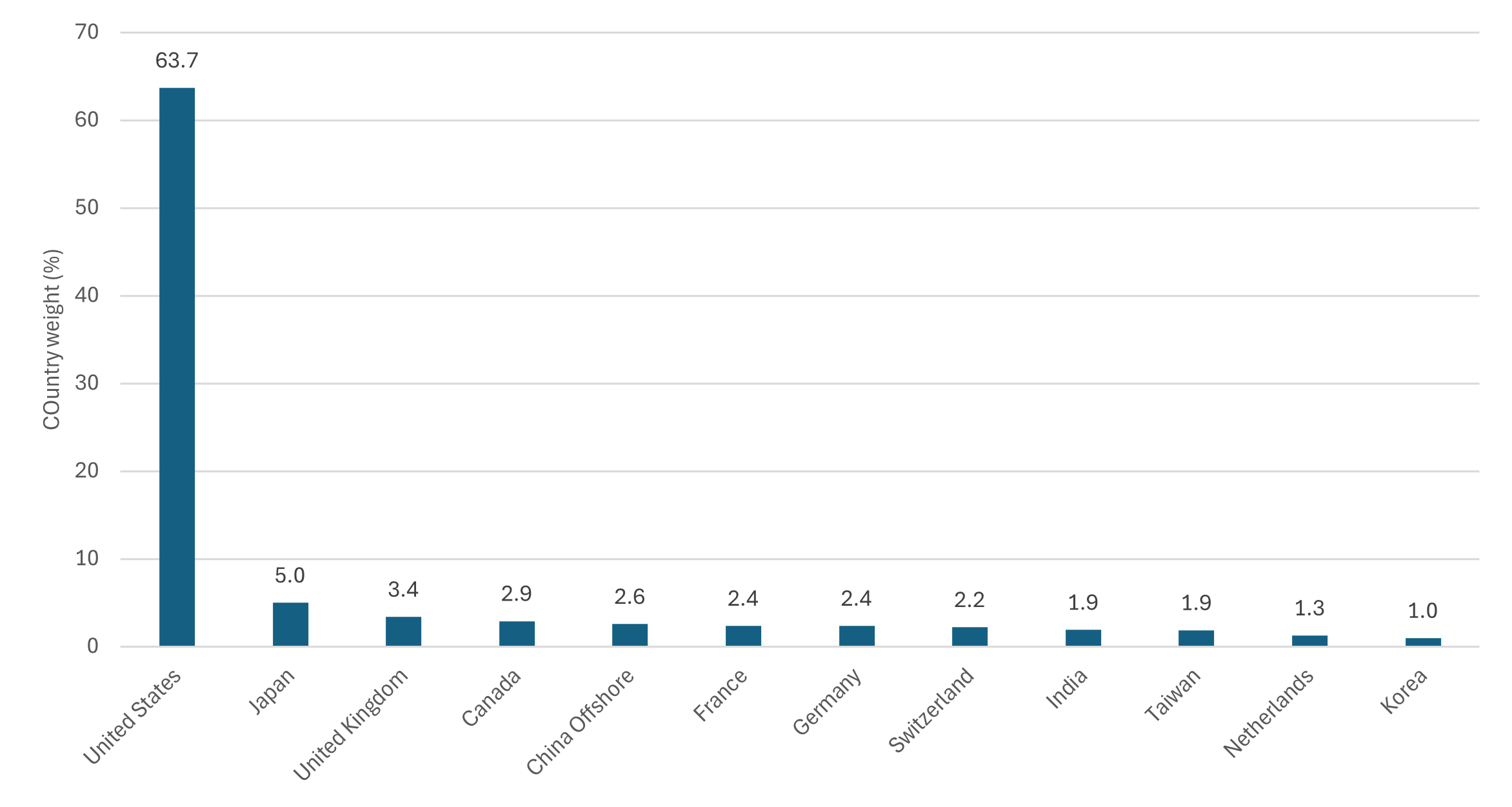

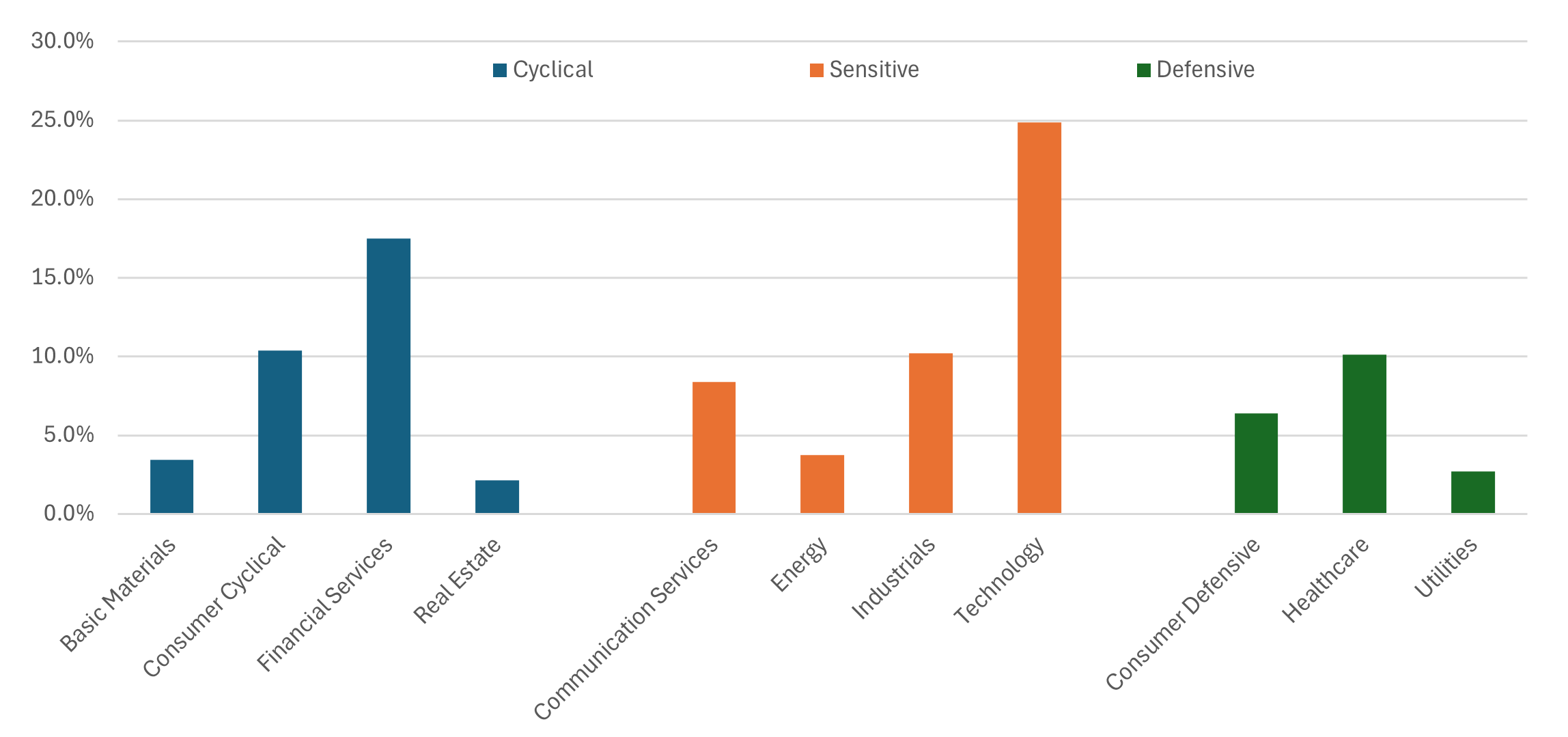

Consider the MSCI All Country World Index (ACWI), the dominant benchmark for global equities. Over 60% of the index is allocated to US equities, with more than 10% concentrated in five companies (See Exhibit 1). Sector weights are skewed heavily toward technology and communications (See Exhibit 2). Growth dominates as a style, and unhedged USD exposure is implicit in the structure. Each of these elements introduces directional risk – to interest rates, to the business cycle, to regulation, and to currency – even if the allocation is described as neutral.

While many large companies operate globally, the structure of market-cap indices still reflects the geography of listings. These indices carry embedded exposure to domestic currency, regulation, and macro policy – factors that may not align with the global footprint of underlying businesses. A regional allocation does not presume that companies are tied to local demand, but rather recognises that capital markets reflect region-specific combinations of risk, policy, and capital formation.

Exhibit 1: MSCI ACWI country composition (largest countries >1% allocation only)

Source: BlackRock Aladdin, Bank of Singapore.

Exhibit 2: MSCI ACWI sector composition

Source: BlackRock Aladdin, Bank of Singapore.

This pattern of concentration reflects a particular regime: one in which falling rates, US tech leadership, and capital-light scalability have been dominant forces. That regime has been favourable to large-cap US equities, and index composition evolved accordingly. But a portfolio shaped by past winners is not necessarily equipped for the next cycle – especially in an environment marked by policy divergence, regional reindustrialisation, and shifting growth drivers.

The implications are practical. A market-cap weighted equity portfolio is not diversified across macro regimes, styles, or currencies. It assumes the continuity of US dominance, tech-driven profitability, and USD strength. These are not baselines; they are embedded bets.

In this sense, market cap is less a neutral benchmark than a trailing narrative. And in a world where forward-looking uncertainty is increasing – across policy, geopolitics, and capital formation – it is worth re-examining what role such a structure should play in a strategic allocation.

The new global regime: Why the world has changed

The case for rethinking equity allocation begins with recognising that the macro environment underpinning global markets has changed. The post-Cold War era – marked by US-led globalisation, disinflation, and deepening financial integration – is giving way to a more fragmented and regionally driven order. Capital remains global, but its flow is increasingly shaped by domestic policy, geopolitical alignment, and supply chain redesign.

These are not cyclical shifts, but structural ones, which Bank of Singapore has written on extensively – most recently in our 2025 Supertrends - Rethinking Portfolios Reimagining the world (July 2025).

One feature of the new regime is the rise of multipolar power centres, each with distinct macroeconomic conditions, institutional frameworks, and strategic objectives. The US, China, India, the European Union (EU), and Japan now influence global markets not just as trading blocs, but as policymakers driving capital formation through domestic industrial strategies. This dispersion of influence is mirrored in the capital markets, where the alignment between geopolitical blocs and financial flows is becoming more explicit.

The return of the state as an economic actor is another defining feature. Public investment, industrial policy, and strategic subsidies are driving capital flows. Defence spending, digital infrastructure, and climate transition are being pursued not only for economic reasons but for security, sovereignty, and strategic competitiveness. These policy initiatives are regionally rooted – and so are their equity market beneficiaries.

At the same time, currency dynamics are becoming less unipolar. The USD remains dominant, but its role as the default global denominator is being gradually eroded by diversification in trade settlement, reserve holdings, and cross-border capital flows. This has implications for portfolio construction – particularly for those built on the implicit assumption of USD strength and stability.

Finally, growth itself is also diverging. The synchronised global cycle of the early 2000s has fractured. Today’s growth trajectories vary meaningfully by region – driven by demographics, fiscal capacity, institutional frameworks, and energy exposure. This makes capital more sensitive to local policy and less tethered to a global beta.

Together, these developments point to a world that is no longer organised around a single axis of growth, risk, or return. In such a regime, portfolios that lean too heavily on one market, one currency, or one style are less resilient – not because those exposures are wrong, but because they no longer represent the world as it is evolving.

For strategic asset allocation, this calls for a broader lens. It requires investors to reconsider the underlying structure of the world that drives expected investment returns and risk. Regional equity allocation becomes a way to map that structure – to reflect how economic power, policy autonomy, and investment opportunity are being reshaped.

Regional allocation: A more deliberate and resilient approach

Shifting from a market-cap weighted portfolio to a regionally structured equity allocation is not a tactical view – it is a strategic design choice. It reflects a belief that equity risk should be expressed in ways that are more balanced, better aligned with structural differentiation, and more resilient to a changing world. It requires a disciplined framework for setting allocations that are grounded in capital market assumptions, calibrated for risk, and resilient across regimes.

At Bank of Singapore, regional weights are set through a RO process – a quantitative framework that acknowledges uncertainty in capital market assumptions and macro regimes. Rather than chase a single forecast, it seeks portfolios that perform reasonably well across many.

To quickly recap: rather than relying on a single point estimate of expected returns or volatility, RO recognises that future states of the world are inherently uncertain. It seeks allocations that deliver reasonable performance across a range of plausible macro and market conditions, rather than maximising performance under a single forecast. This is particularly relevant in equity allocation, where regional return distributions are increasingly shaped by policy regimes, geopolitical alignment, and structural growth models.

This approach enables portfolios to avoid inherited concentrations and the resulting regional allocation becomes a way to map structural variation – in growth models, policy priorities, institutional frameworks, and currency regimes – with each region contributing distinct attributes:

The resulting portfolio is more diversified across dimensions often overlooked by market-cap weighting:

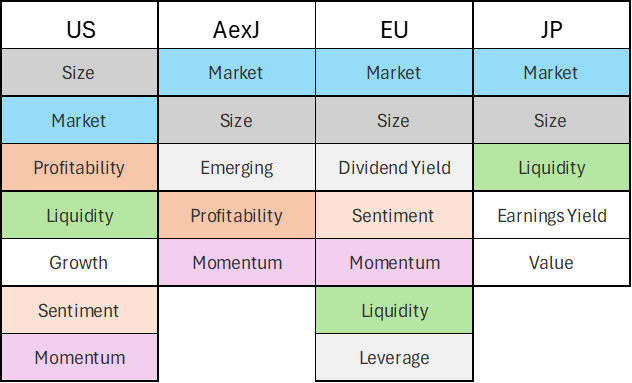

Exhibit 3: Key style exposures in regional equities (in descending order of significance)

Source: BlackRock Aladdin, Bank of Singapore. Style definitions: Market: Captures risk associated with general equity market movements; Size: Company size based on market capitalisation and fundamental data; Momentum: Longer-term trend in stock prices over the last year; Liquidity: Various measures of trading activity and price impact; Value: Identifies cheap vs. expensive stocks relative to fundamentals; Earnings Yield: Earnings-to-price & related measures; Dividend Yield: Dividend-to-price; Profitability: Return on equity (ROE) and related measures; Growth: Historical growth in assets & sales; Leverage: Various measures of indebtedness; Sentiment: Sensitivity of stock return with changes in the VIX index.

This approach is a structural rebalancing – a way to express equity exposure in a way that reflects plausible future states of the world, and not just where capital has accumulated. Through RO and regional logic, the equity sleeve becomes better positioned for resilience across a range of outcomes.

When does this outperform? When might it lag?

With the regional structure in place, it is important to understand how such a portfolio tends to behave across different conditions, particularly relative to standard global equity reference point (MSCI ACWI).

The following return patterns describe how the regional sleeve has historically performed relative to MSCI ACWI, under different macro and market conditions.

When the allocation tends to outperform

When global growth is not dominated by the US but instead distributed across Asia, Europe and Japan – often driven by manufacturing, infrastructure, or policy investment – the regional sleeve benefits from its balanced exposure.

Non-US equities gains from local currency strength during periods of broad USD depreciation or FX dispersion.

The regional sleeve has less exposure to growth-heavy US tech and more to financials, exporters, and industrials. It benefits when leadership rotates away from high-duration growth stocks.

Themes such as climate transition, infrastructure, and industrial policy often show up more clearly in Asia and Europe. These regions gain when global capital formation is driven by government policy or real asset investment.

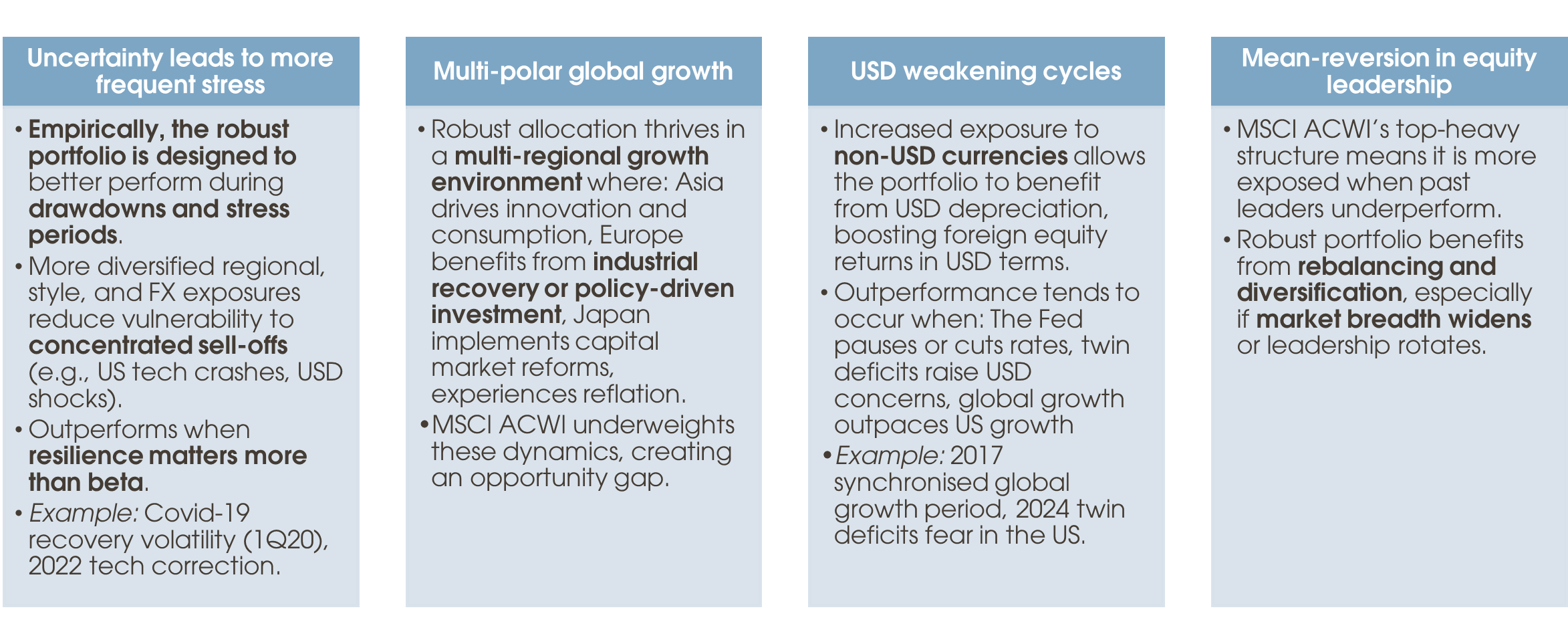

The following Exhibit 4 summarises how the regionally diversified portfolio is better positioned in a climate of radical uncertainty, secular changes to growth and the USD, and given the limited longevity of equity leadership.

Exhibit 4: A more regionally diversified equity portfolio can capitalise on key secular shifts

Source: Bank of Singapore.

When the allocation may lag

Periods where US earnings, innovation, or macro policy dominate can lead to concentrated market-cap index outperformance – particularly if leadership is narrow and index-heavy.

With meaningful unhedged exposure to non-USD currencies, the regional allocation may underperform when the USD strengthens materially – historically this has happened during global stress. This sometimes may only reflect the currency translation effects on local equity returns, even if underlying fundamentals remain sound.

In concentrated bull markets led by a small number of US mega-cap tech stocks, the equity sleeve – by design – has a smaller allocation to the drivers of index-level outperformance.

While this note focuses on asset allocation, it does so with the understanding that long-term equity returns are driven by the underlying earnings power of listed companies. Security selection remains critical. The role of regional allocation is to create a structure that reflects differentiated sources of return and risk–allowing stock selection to operate within a more balanced and resilient investment universe.

A portfolio built for balance, not bets

These return patterns do not define success or failure, and they have been assessed over shorter horizons than the intended duration of an SAA. The regional equity sleeve is constructed not to outperform in any specific regime, but to avoid overexposure to any one of them. It reduces reliance on the persistence of US tech dominance, embeds natural currency and style diversification, and increases sensitivity to global – rather than US-centric – capital formation.

In a world shaped by multiple growth models, policy regimes, and macro uncertainties, that balance is not just defensive. It is forward aligned.

Disclaimers and Disclosures

This material is prepared by Bank of Singapore Limited (Co Reg. No.: 197700866R) (the “Bank”) and is distributed in Singapore by the Bank.

This material does not provide individually tailored investment advice. This material has been prepared for and is intended for general circulation. The contents of this material does not take into account the specific investment objectives, investment experience, financial situation, or particular needs of any particular person. You should independently evaluate the contents of this material, and consider the suitability of any product discussed in this material, taking into account your own specific investment objectives, investment experience, financial situation and particular needs. If in doubt about the contents of this material or the suitability of any product discussed in this material, you should obtain independent financial advice from your own financial or other professional advisers, taking into account your specific investment objectives, investment experience, financial situation and particular needs, before making a commitment to purchase any product.

The Bank shall not be responsible or liable for any loss (whether direct, indirect or consequential) that may arise from, or in connection with, any use of or reliance on any information contained in or derived from this material, or any omission from this material, other than where such loss is caused solely by the Bank’s wilful default or gross negligence.

This material is not and should not be construed, by itself, as an offer or a solicitation to deal in any product or to enter into any legal relations. You should contact your own licensed representative directly if you are interested in buying or selling any product discussed in this material.

This material is not intended for distribution, publication or use by any person in any jurisdiction outside Singapore, Hong Kong or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank or its related corporations, connected persons, associated persons or affiliates (collectively “Affiliates”) to any licensing, registration or other requirements in such jurisdiction.

The Bank and its Affiliates may have issued other reports, analyses, or other documents expressing views different from the contents of this material, and may provide other recommendations or make investment decisions that are contrary to the views expressed in this material, and all views expressed in all reports, analyses and documents are subject to change without notice. The Bank and its Affiliates reserve the right to act upon or use the contents of this material at any time, including before its publication.

The author of this material may have discussed the information or views contained in this material with others within or outside the Bank, and the author or such other Bank employees may have already acted on the basis of such information or views (including communicating such information or views to other customers of the Bank).

The Bank, its employees (including those with whom the author may have consulted in the preparation of this material))and discretionary accounts managed by the Bank may have long or short positions (including positions that may be different from or opposing to the views in this material or may be otherwise interested in any of the product(s) (including derivatives thereof) discussed in material, may have acquired such positions at prices and market conditions that are no longer available, may from time to time deal in such product(s) and may have interests different from or adverse to your interests.

Analyst Declaration

The analyst(s) who prepared this material certifies that the opinions contained herein accurately and exclusively reflect his or her views about the securities of the company(ies) and that he or she has taken reasonable care to maintain independence and objectivity in respect of the opinions herein.

The analyst(s) who prepared this material and his/her associates do not have financial interests in the company(ies). Financial interests refer to investments in securities, warrants and/or other derivatives. The analyst(s) receives compensation based on the overall revenues of Bank of Singapore Limited, and no part of his or her compensation was, is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this material. The reporting line of the analyst(s) is separate from and independent of the business solicitation or marketing departments of Bank of Singapore Limited.

The analyst(s) and his/her associates confirm that they do not serve as directors or officers of the company(ies) and the company(ies)or other third parties have not provided or agreed to provide any compensation or other benefits to the analyst(s) in connection with this material.

An “associate” is defined as (i) the spouse, parent or step-parent, or any minor child (natural or adopted) or minor step-child, or any sibling or step-sibling of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, parent or step-parent, minor child (natural or adopted) or minor step-child, or sibling or step-sibling is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

Conflict of Interest Declaration

The Bank is a licensed bank regulated by the Monetary Authority of Singapore in Singapore. Bank of Singapore Limited, Hong Kong Branch (incorporated in Singapore with limited liability), is an Authorized Institution as defined in the Banking Ordinance of Hong Kong (Cap 155), regulated by the Hong Kong Monetary Authority in Hong Kong and a Registered Institution as defined in the Securities and Futures Ordinance of Hong Kong (Cap.571) regulated by the Securities and Futures Commission in Hong Kong. The Bank, its employees and discretionary accounts managed by its Singapore Office/Hong Kong Office may have long or short positions or may be otherwise interested in any of the investment products (including derivatives thereof) referred to in this document and may from time to time dispose of any such investment products. The Bank forms part of the OCBC Group (being for this purpose Oversea-Chinese Banking Corporation Limited (“OCBC Bank”) and its subsidiaries, related and affiliated companies). OCBC Group, their respective directors and/or employees (collectively “Related Persons”) may have interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. OCBC Group and its Related Persons may also be related to, and receive fees from, providers of such investment products. There may be conflicts of interest between OCBC Bank, the Bank, OCBC Investment Research Private Limited, OCBC Securities Private Limited or other members of the OCBC Group and any of the persons or entities mentioned in this report of which the Bank and its analyst(s) are not aware due to OCBC Bank’s Chinese Wall arrangement.

The Bank adheres to a group policy (as revised and updated from time to time) that provides how entities in the OCBC Group manage or eliminate any actual or potential conflicts of interest which may impact the impartiality of research reports issued by any research analyst in the OCBC Group.

Other Disclosures

Dubai International Financial Center (DIFC)

Where this material relates to structured products and bonds, this clause applies:

The Distributor represents and agrees that it has not offered and will not offer the product to any person in the Dubai International Financial Centre unless such offer is an “Exempt Offer” in accordance with the Market Rules of the Dubai Financial Services Authority (the “DFSA”).

The DFSA has no responsibility for reviewing or verifying any documents in connection with Exempt Offers.

The DFSA has not approved the Information Memorandum or taken steps to verify the information set out in it, and has no responsibility for it.

The product to which this document relates may be illiquid and/or subject to restrictions in respect of their resale. Prospective purchasers of the products offered should conduct their own due diligence on the products.

Please make sure that you understand the contents of the relevant offering documents (including but not limited to the Information Memorandum or Offering Circular) and the terms set out in this document. If you do not understand the contents of the relevant offering documents and the terms set out in this document, you should consult an authorised financial adviser as you deem necessary, before you decide whether or not to invest.

Where this material relates to a fund, this clause applies:

This Fund is not subject to any form of regulation or approval by the Dubai Financial Services Authority (“DFSA”). The DFSA has no responsibility for reviewing or verifying any Prospectus or other documents in connection with this Fund. Accordingly, the DFSA has not approved the Prospectus or any other associated documents nor taken any steps to verify the information set out in the Prospectus, and has no responsibility for it. The Units to which this Fund relates may be illiquid and/or subject to restrictions on their resale. Prospective purchasers should conduct their own due diligence on the Units. If you do not understand the contents of this document you should consult an authorized financial adviser. Please note that this offer is intended for only Professional Clients and is not directed at Retail Clients.

These are also available for inspection, during normal business hours, at the following location:

Bank of Singapore

Office 30-34 Level 28

Central Park Tower

DIFC, Dubai

U.A.E

Hong Kong

Bank of Singapore Limited (Hong Kong Branch) is an Authorized Institution as defined in the Banking Ordinance of Hong Kong (Cap 155), regulated by the Hong Kong Monetary Authority in Hong Kong and a Registered Institution as defined in the Securities and Futures Ordinance of Hong Kong (Cap.571). Financial products and services are only offered to “Professional Investors" within the meaning of the Securities and Futures Ordinance and the Securities and Futures (Professional Investor) Rules made thereunder.

This material has not been delivered for registration to the Registrar of Companies in Hong Kong and its contents have not been reviewed by any regulatory authority in Hong Kong. Accordingly: (i) the investment product may not be offered or sold in Hong Kong by means of any document other than to persons who are "Professional Investors" within the meaning of the Securities and Futures Ordinance (Cap. 571) of Hong Kong and the Securities and Futures (Professional Investor) Rules made thereunder or in other circumstances which do not result in the document being a "prospectus" within the meaning of the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Cap. 32) of Hong Kong or which do not constitute an offer to the public within the meaning of the Companies (Winding Up and Miscellaneous Provisions) Ordinance; and (ii) no person may issue any invitation, advertisement or other material relating to the investment product whether in Hong Kong or elsewhere, which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong (except if permitted to do so under the securities laws of Hong Kong) other than with respect to the investment product which is or is intended to be disposed of only to persons outside Hong Kong or only to "Professional Investors" within the meaning of the Securities and Futures Ordinance and the Securities and Futures (Professional Investor) Rules made thereunder.

Where this material involves derivatives, do not invest in it unless you fully understand and are willing to assume the risks associated with it. If you have any doubt, you should seek independent professional financial, tax and/or legal advice as you deem necessary.

Where this material relates to a Complex Product, this clause applies:

Warning Statement and Information about Complex Product

(Applicable to accounts managed by Hong Kong Relationship Managers)

Where this material relates to a Complex Product (funds and ETFs), this clause applies additionally:

Where this material relates to a Complex Product (Options and its variants, Swap and its variants, Accumulator and its variants, Reverse Accumulator and its variants, Forwards), this clause applies additionally:

Where this material relates to a Loss Absorption Product, this clause applies:

Warning Statement and Information about Loss Absorption Products

(Applicable to accounts managed by Hong Kong Relationship Managers)

Before you invest in any Loss Absorption Product (as defined by the Hong Kong Monetary Authority), please read and ensure that you understand the features of a Loss Absorption Product, which may generally have the following features:

Where this material relates to a certificate of deposit, this clause applies:

A certificate of deposit is not a protected deposit and is not protected by the Deposit Protection Scheme in Hong Kong.

Where this material relates to a structured deposit, this clause applies:

A structured deposit is not a protected deposit and is not protected by the Deposit Protection Scheme in Hong Kong.

Where this material relates to a structured product, this clause applies:

This is a structured product which involves derivatives. Do not invest in it unless you fully understand and are willing to assume the risks associated with it. If you are in any doubt about the risks involved in the product, you may clarify with the intermediary or seek independent professional advice.

Singapore

Bank of Singapore Limited is a bank licensed and regulated by the Monetary Authority of Singapore. The Bank is also an Exempt Capital Markets Services Entity under the Securities and Futures Act 2001 and an Exempt Financial Adviser under the Financial Advisers Act 2001.

Where this material relates to structured deposits, this clause applies:

The product is a structured deposit. Structured deposits are not insured by the Singapore Deposit Insurance Corporation. Unlike traditional deposits, structured deposits have an investment element and returns may vary. You may wish to seek independent advice from a financial adviser before making a commitment to purchase this product. In the event that you choose not to seek independent advice from a financial adviser, you should carefully consider whether this product is suitable for you.

Where this material relates to dual currency investments, this clause applies:

The product is a dual currency investment. A dual currency investment product (“DCI”) is a derivative product or structured product with derivatives embedded in it. A DCI involves a currency option which confers on the deposit-taking institution the right to repay the principal sum at maturity in either the base or alternate currency. Part or all of the interest earned on this investment represents the premium on this option.

By purchasing this DCI, you are giving the issuer of this product the right to repay you at a future date in an alternate currency that is different from the currency in which your initial investment was made, regardless of whether you wish to be repaid in this currency at that time. DCIs are subject to foreign exchange fluctuations which may affect the return of your investment. Exchange controls may also be applicable to the currencies your investment is linked to. You may incur a loss on your principal sum in comparison with the base amount initially invested. You may wish to seek advice from a financial adviser before making a commitment to purchase this product. In the event that you choose not to seek advice from a financial adviser, you should carefully consider whether this product is suitable for you.

United Kingdom

Bank of Singapore Limited, UK Branch (BOSL UK) is incorporated and registered in Singapore with the Accounting and Corporate Regulatory Authority (Registration no.:197700866R) as a public company limited by shares with head office in Singapore and operating in the UK through its UK establishment (BR027666). Bank of Singapore Limited, UK branch (FRN: 1038970) is an appointed representative of Oversea-Chinese Banking Corporation Limited, London branch. Oversea-Chinese Banking Corporation Limited (OCBC) is authorised and regulated by the Monetary Authority of Singapore. OCBC London Branch is authorised by the Prudential Regulation Authority with firm reference number 204687 and subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of OCBC London Branch’s regulation by the Prudential Regulation Authority are available on request. This material is intended solely for the use of the designated recipients. Unauthorised access, use, or distribution is strictly prohibited. If you are not the intended recipient, please notify us immediately and erase all copies. Bank of Singapore Limited, UK Branch does not provide legal, accounting or tax advice. Please consult an independent professional for advice tailored to your specific situation.

This product or service is offered exclusively for investors eligible for categorisation as a professional client. This is not intended for retail clients. Any person in the UK who receives this material is deemed to have represented and agreed that they qualify as a Professional Client. Such recipients also represent and agree that they have not received this material on behalf of any persons in the UK other than Professional Clients for whom they have authority to make investment decisions on a wholly discretionary basis. BOSL UK will rely on the truth and accuracy of these representations and agreements. Any person who is not a Professional Client should neither act on nor rely upon this material or any of its contents.

Investing in financial markets carries the risk of losing capital, and investors should be aware of and carefully consider this risk before making any investment decisions. The value of investments can fluctuate, and there is no guarantee that investors will recoup their initial investment. Past performance is not indicative of future results, and the performance of investments can be affected by various factors, including but not limited to market conditions, economic factors, and changes in regulations or tax laws. Forward-looking statements should not be considered as guarantees or predictions of future events. Investors should be prepared for the possibility of losing all or a portion of their invested capital. It is recommended that investors seek professional advice and conduct thorough research before making any investment decisions. BOSL UK does not endorse any specific investments or financial products mentioned in this material. Neither BOSL UK nor its employees accept any liability for any loss or damage arising from the use of this material or reliance on its content.

Cross Border Disclaimer and Disclosures

Refer to https://www.bankofsingapore.com/Disclaimers_and_Disclosures.html for cross-border marketing disclaimers and disclosures.

ESG Disclaimer

This document contains information on ESG factors or the Bank’s process for taking into consideration, and evaluation or assessment of ESG factors.

There are currently no universally accepted environmental, social and governance (“ESG”) standards, and no consensus as to whether activities and practices or products or services are “environmentally friendly”, “sustainable”, “responsible”, “climate friendly”, etc. Evaluation of ESG outcomes or metrics may require forward-looking scenario analysis, estimates, interpretations and assumptions and may be uncertain and speculative. There may not be scientific consensus. Scientific evidence and data may not be conclusive or there may be limitations, and new evidence and data may be emerging. ESG standards may depend on subjective or value judgments. ESG standards, as well as laws, rules and regulations may differ from jurisdiction to jurisdiction. Taxonomies have been developed in different jurisdictions to classify activities as “environmentally sustainable”, “green” or the equivalent, and different taxonomies may classify the same activity differently. Achieving one ESG goal may be at the expense of, or require a compromise on, other ESG goals. The Bank’s ESG standards and evaluation or assessment of ESG factors may therefore not meet your expectations or objectives and may not be consistent with certain ESG laws, rules, regulations and standards. There is no guarantee that there will not be negative ESG outcomes, and the Bank does not give any assurance that your investments will have a positive ESG impact. You should ensure that you understand the Bank’s ESG standards and process for evaluation or assessment of ESG factors, and assess whether the Bank’s ESG standards and process for evaluation or assessment of ESG factors meets your expectations or is appropriate for you, before making any investment commitment. You are solely responsible for your own investment decisions.

The Bank relies on third party ESG ratings. While the Bank has selected its third party ESG rating providers in good faith and with reasonable care, the Bank has not independently verified the ESG ratings of third party providers. The Bank gives no representation or warranty, express or implied, as to the quality, accuracy, completeness, rigour, timeliness or verifiability of such third party ESG ratings, and shall not be responsible or liable for such third party ESG ratings. ESG ratings may be based on data that is incomplete, due to limitations or otherwise, or based on commitments and targets which may not be achieved. You should review and understand the disclosures made by such third party ESG ratings providers on their methodologies, data sources and other relevant information, and obtain advice from professional advisers as necessary.

Taking into consideration ESG factors may be at the expense of higher financial returns, especially in the short term. Although ESG risks may result in financial losses, such losses may, and if at all, only materialise in the long term. ESG factors and screening may also result in certain investments that deliver high financial returns being excluded, or limit the diversity of investments, which could in turn affect the volatility of portfolios.