After rallying through the second half of 2020, the EUR appears to have run aground in 2021. Slow vaccination rollout and the European Central Bank’s (ECB) resistance to rising yields have undermined the EUR.

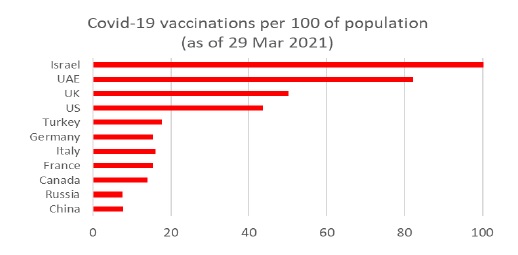

The European Union’s (EU) sluggish vaccine roll-out, along with a succession of lockdowns, is one of the major surprises of 2021. The pandemic has yet to relax its grip, forcing several countries to extend their lockdowns yet again. At the same time, production of and access to vaccines in the EU have been frustratingly slow.

Eurozone lags while the US and UK lead in vaccination progress

Source: Our World in Data, Bank of Singapore

There are undoubtedly fears that Europe will miss out on the all-important summer hospitality season. If Covid-19 restrictions mean that much of Europe is not going on holiday on airplanes, Eurozone growth expectations could trail the bounce in US growth that is levered to unprecedented fiscal stimulus and mass vaccinations ramping up. It is this shift in relative growth expectations against the Euro area in favour of the US that has pushed the EURUSD lower.

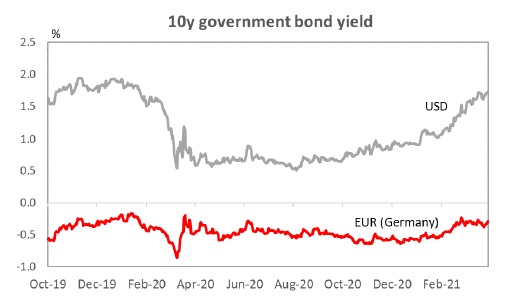

The divergence in G10 yields has also emboldened the EUR’s status as a preferred funding currency over the USD this year. On one hand, Fed Chair Powell's ambivalence regarding higher US Treasury yields suggests that the Fed endorses steeper yield curves as a reflection of stronger growth outlook. By contrast, the ECB made it clear they will push back against rising yields. The ECB recently announced a temporary acceleration of bond purchases under the Pandemic Emergency Purchase Programme (PEPP) to attempt to decouple European yields from the US. That said, the pushback against rising European yields should ease once the European economic recovery takes hold.

Divergence between European and US yields has weighed on the EURUSD this year

Divergence between European and US yields has weighed on the EURUSD this year

Source: Bloomberg, Bank of Singapore

A sustained EUR weakness is still premature. But with Europe’s economic rebound likely tempered by Covid-19, we update the 12-month EURUSD forecast to 1.25 (old: 1.30) to reflect less upside.

While the EU’s vaccination campaign has lagged behind other regions, that process should begin to accelerate in the next 1-2 months. Problems with vaccine distribution have added to European woes, but better-than-expected March Eurozone PMI data illustrate how much pent-up consumer demand is waiting to be unleashed once inoculations become more widespread.

We would therefore caution against extrapolating EURUSD weakness too far in the near-term. It is also hard to see a more persistent rebound in the USD given that US monetary conditions will remain loose and global risk appetite will remain supported. As vaccination progress accelerates, this should pave way for greater growth-to-value rotation and the resulting equity inflows could support modest EURUSD upside in the medium-term.