en-sg

Search

Aa

Large

Medium

Small

English

English

繁體中文

简体中文

Client Login

Solutions

Back

Solutions

Find out all solutions

We serve

Individuals

Family offices

Financial intermediaries

We help you

Grow your wealth

Secure your legacy

Explore financing solutions

Find out all solutions

Insights

Back

Insights

Discover all insights

Read

CIO insights

Stories

Watch

Market Watch

Listen

Podcast

Discover all insights

Events

Back

Events

Check out all events

Spotlight

In Conversation With

Arts and Culture

Sustainability

The Outlook Ahead

Beyond

Mid-year Outlook

Check out all events

About us

Back

About us

See all about us

Our leadership team

CIO Investment Institute

Our branches and subsidiaries

Media

Press release

Notice

See all about us

Careers

Back

Careers

Build your career with us

Students and graduates

Internship Programme

Corporate Analyst Programme

Wealth Management Programme

Build your career with us

Contact us

Aa

Back

Aa

Large

Medium

Small

SG/EN

Back

English

English

繁體中文

简体中文

Close

All insights

Home

Insights

All insights

Explore our solutions

Discover investment solutions, wealth planning and more.

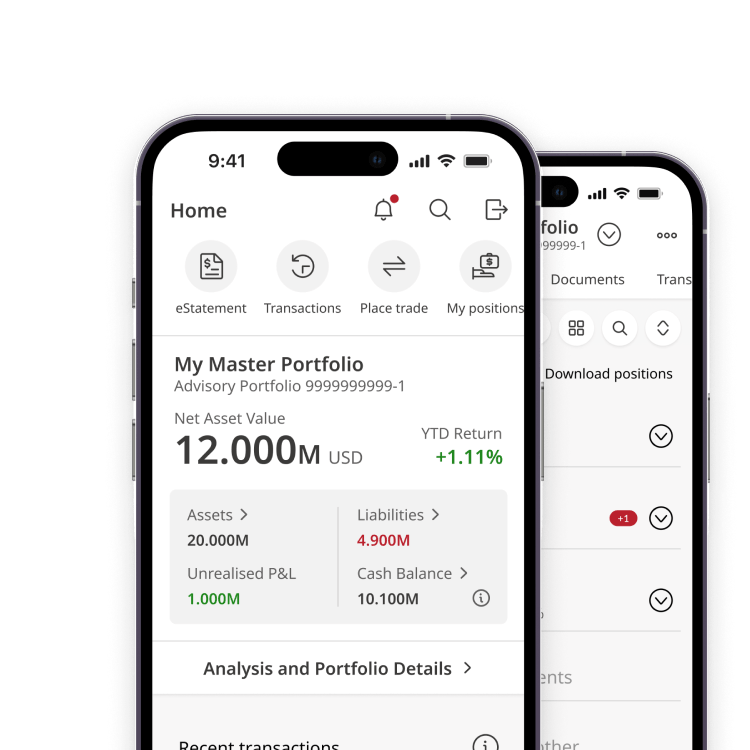

Capture wealth opportunities on the go

Make informed decisions in real time with our Digital Services app.

Access our insights

Learn about intergenerational wealth and navigating family office challenges.

Was this page useful?

Great! What did you like about this page?

Subject matter expertise

Topic relevance

Timeliness

Content format

Others

Comment (optional)

Submit

Sorry to hear that. How can we improve this page?

Subject matter expertise

Topic relevance

Timeliness

Content format

Others

Comment (optional)

Submit

Thank you for your feedback

We will use your feedback to improve your content experience.

Unable to send response

We’re having trouble submitting your response. Please try again.

Try again

Scan the QR code with WeChat

Close