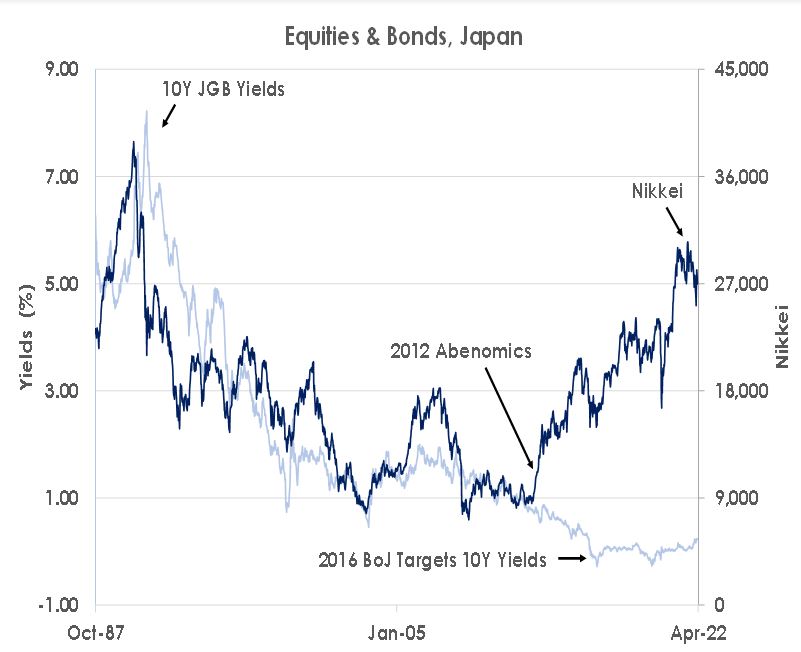

The JPY is trading at a 20-year low of 126 against the USD. The dovish Bank of Japan is capping 10Y Japanese Government Bond (JGB) yields ‘around 0%’ - as the first chart shows - to push inflation up to its 2% target while the Federal Reserve is ready for 50bps hikes to curb inflation.

Source: Bank of Singapore, Bloomberg.

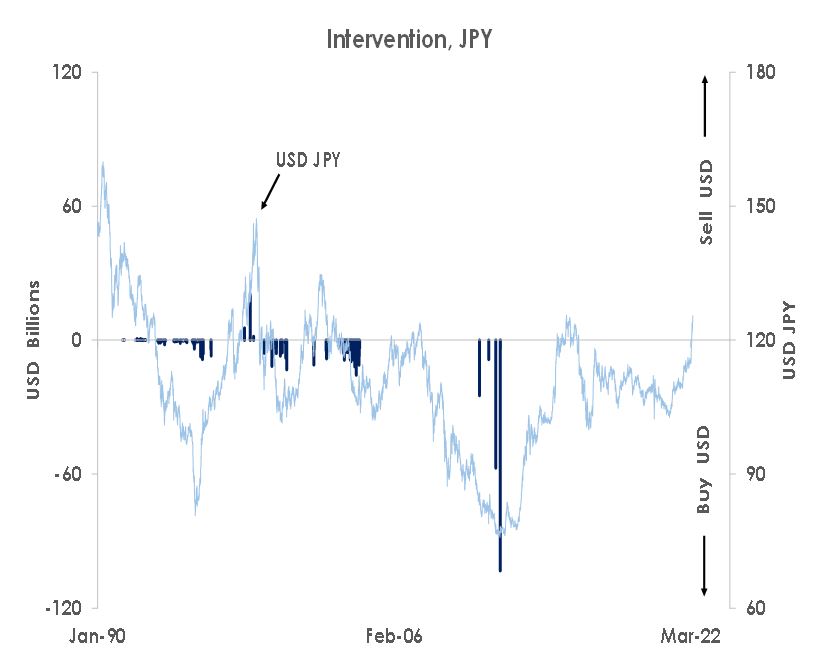

If the JPY keeps weakening, the BoJ - on behalf of the Ministry of Finance - could intervene to support the currency by drawing down its foreign exchange reserves. But the last time Tokyo acted to defend the JPY by selling USDs was in 1998 when the currency fell into a 130-140 range before finally hitting a low of 148 as the second chart shows. We think officials will only intervene now in the currency markets if the JPY plunges into a 130-140 range again versus the USD.

Source: Bank of Singapore, Bloomberg.

Instead, the larger risk to JPY bears would be if the BoJ suddenly lifts its JGB target, enabling 10Y yields to rise above their current cap at 0.25%. Japanese yields would likely surge - as global yields have this year on inflation fears - causing the JPY to rebound sharply.

Source: Bank of Singapore, Bloomberg.

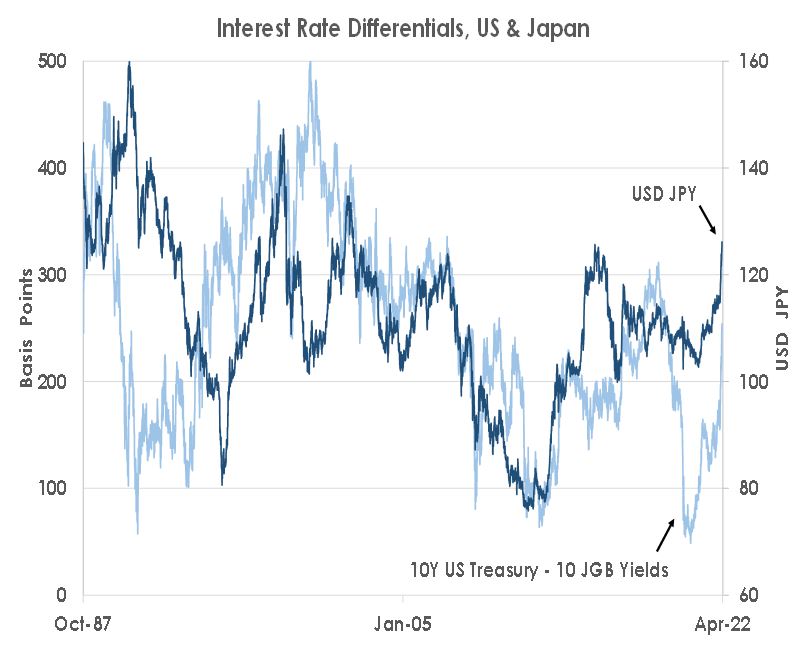

If the falling JPY keeps raising the cost of energy imports, then the BoJ may be tempted to let JGB yields rise. This would narrow the gap with US yields to the JPY’s benefit as the last chart shows. But a sudden change in the JGB yield target could induce a major shock as the Swiss National Bank’s removal of its CHF cap did in 2015. We doubt Governor Kuroda would take such a risk before his retires next year, especially as inflation in Japan is finally near the 2% goal he set in 2013.

Important information

This product may only be offered: (i) in Hong Kong, to qualified Private Banking Customers and Professional Investors (as defined under the Securities and Futures Ordinance); and (ii) in Singapore, to Accredited Investors (as defined under the Securities and Futures Act) and (iii) in the Dubai International Financial Center to Professional Clients (as defined under the Dubai Financial Services Authority rules) only. No other person should act on the contents of this document.This product may involve derivatives. Do NOT invest in it unless you fully understand and are willing to assume the risks associated with it. If you have any doubt, you should seek independent professional financial, tax and/or legal advice as you deem necessary.

Please carefully read and make sure that you understand all Risk Disclosures, Selling Restrictions, and Disclaimers. This document must be read together with the relevant Prospectus & Offering Documents &/or Key Fact Statement.

Disclaimer

This document is prepared by Bank of Singapore Limited (Co Reg. No.: 197700866R) (the “Bank”), is for information purposes only, and is not, by itself, intended for anyone other than the recipient. It may contain information proprietary to the Bank which may not be reproduced or redistributed in whole or in part without the Bank’s prior consent. It is not an offer or a solicitation to deal in any of the investment products referred to herein or to enter into any legal relations, nor an advice or by itself a recommendation with respect to such investment products. It does not have regard to the specific investment objectives, investment experience, financial situation and the particular needs of any recipient or customer. Customers should exercise caution in relation to any potential investment. Customers should independently evaluate each investment product and consider the suitability of such investment product, taking into account customer’s own specific investment objectives, investment experience, financial situation and/or particular needs. Customers will need to decide on their own as to whether or not the contents of this document are suitable for them. If a customer is in doubt about the contents of this document and/or the suitability of any investment products mentioned in this document for the customer, the customer should obtain independent financial, legal and/or tax advice from its professional advisers as necessary, before proceeding to make any investments.

The Bank, its Affiliates and their respective employees are not in the business of providing, and do not provide, tax, accounting or legal advice to any clients. The material contained herein is prepared for informational purposes and is not intended or written to be used, and cannot be used or relied upon for tax, accounting or legal advice. Any such client is responsible for consulting his/her own independent advisor as to the tax, accounting and legal consequences associated with his/her investments/transactions based on the client’s particular circumstances.

This document and other related documents have not been reviewed by, registered or lodged as a prospectus, information memorandum or profile statement with the Monetary Authority of Singapore nor any regulator in Hong Kong or elsewhere.

This document may not be published, circulated, reproduced or distributed in whole or in part to any other person without the Bank’s prior written consent. This document is not intended for distribution to, publication or use by any person in any jurisdiction outside Singapore, Hong Kong, or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank and its related corporations, connected persons, associated persons and/or affiliates (collectively, “Affiliates”) to any registration, licensing or other requirements within such jurisdiction.